I believe that the times ahead will be radically different from the times we have experienced so far in our lifetimes, though similar to many other times in history.

I believe this because about 18 months ago I undertook a study of the rises and declines of empires, their reserve currencies, and their markets, prompted by my seeing a number of unusual developments that hadn’t happened before in my lifetime but that I knew had occurred numerous times in history. Most importantly, I was seeing the confluence of 1) high levels of indebtedness and extremely low interest rates, which limits central banks’ powers to stimulate the economy, 2) large wealth gaps and political divisions within countries, which leads to increased social and political conflicts, and 3) a rising world power (China) challenging the overextended existing world power (the US), which causes external conflict. The most recent analogous time was the period from 1930 to 1945. This was very concerning to me.

As I studied history, I saw that this confluence of events was typical of periods that existed as roughly 10- to 20-year transition phases between big economic and political cycles that occurred over many years (e.g., 50-100 years). These big cycles were comprised of swings between 1) happy and prosperous periods in which wealth is pursued and created productively and those with power work harmoniously to facilitate this and 2) miserable, depressing periods in which there are fights over wealth and power that disrupt harmony and productivity and sometimes lead to revolutions/wars. These bad periods were like cleansing storms that got rid of weaknesses and excesses, such as too much debt, and returned the fundamentals to a sounder footing, albeit painfully. They eventually caused adaptations that made the whole stronger, though they typically changed who was on top and the prevailing world order.

The answers to this question can only be found by studying the mechanics behind similar cases in history—the 1930-45 period but also the rise and fall of the British and Dutch empires, the rise and fall of Chinese dynasties, and others—to unlock an understanding of what is happening and what is likely to happen.[1] That was the purpose of this study. Then the pandemic came along, which was another one of those big events that never happened to me but happened many times before my lifetime that I needed to understand better.

My Approach

While it might seem odd that an investment manager who is required to make investment decisions on short time frames would pay so much attention to long-term history, through my experiences I have learned that I need this perspective to do my job well. My biggest mistakes in my career came from missing big market moves that hadn’t happened in my lifetime but had happened many times before. These mistakes taught me that I needed to understand how economies and markets have worked throughout history and in faraway placesso that I could learn the timeless and universal mechanics underlying them and develop timeless and universal principles for dealing with them well.

The first of these big surprises for me came in 1971 when I was 22 years old and clerking on the floor of the New York Stock Exchange as a summer job. On a Sunday night, August 15, 1971, President Nixon announced that the US would renege on its promise to allow paper dollars to be turned in for gold. This led the dollar to plummet. As I listened to Nixon speak, I realized that the US government had defaulted on a promise and that money as we knew it had ceased to exist. That couldn’t be good, I thought. So on Monday morning I walked onto the floor of the exchange expecting pandemonium as stocks took a dive. There was pandemonium all right, but not the sort I expected. Instead of falling, the stock market jumped about 4 percent. I was shocked. That is because I hadn’t experienced a currency devaluation before. In the days that followed, I dug into history and saw that there were many cases of currency devaluations that had similar effects on stock markets. By studying further, I figured out why, and I learned something valuable that would help me many times in my future. It took a few more of those painful surprises to beat into my head the realization that I needed to understand all the big economic and market moves that had happened in the last 100+ years and in all major countries.

In other words, if some big and important event had happened in the past (like the Great Depression of the 1930s), I couldn’t say for sure that it wouldn’t happen to me, so I had to figure out how it worked and be prepared to deal with it well. Through my research I saw that there were many cases of the same type of thing happening (e.g., depressions) and that by studying them just like a doctor studies many cases of a particular type of disease, I could gain a deeper understanding of how they work. The way I work is to study as many of the important cases of a particular thing I can find and then to form a picture of a typical one, which I call an archetype. The archetype helps me see the cause-effect relationships that drive how these cases typically progress. Then I compare how the specific cases transpire relative to the archetypical one to understand what causes the differences between each case and the archetype. This process helps me refine my understanding of the cause-effect relationships to the point where I can create decision-making rules in the form of “if/then” statements—i.e., if X happens, then make Y bet. Then I watch actual events transpire relative to that template and what we are expecting. I do these things in a very systematic way with my partners at Bridgewater Associates.[1a] If events are on track we continue to bet on what typically comes next, and if events start to deviate we try to understand why and course correct.

My approach is not an academic one created for scholarly purposes; it is a very practical one that I follow in order to do my job well. You see, as a global macro investor, the game I play requires me to understand what is likely to happen to economies better than the competition does. From my years of wrestling with the markets and trying to come up with principles for doing it well, I’ve learned that 1) one’s ability to anticipate and deal well with the future depends on one’s understanding of the cause-effect relationships that make things change and 2) one’s ability to understand these cause-effect relationships comes from studying how they have played out in the past. How practical this approach has been can be measured in Bridgewater’s performance track record over several decades.

This Approach Affects How I See Everything

Having done many such studies in pursuit of timeless and universal principles, I’ve learned that most things—e.g., prosperous periods, depressions, wars, revolutions, bull markets, bear markets, etc.—happen repeatedly through time. They come about for basically the same reasons, typically in cycles, and often in cycles that are as long or longer than our lifetimes. This has helped me come to see most everything as “another one of those,” just like a biologist, upon encountering a creature in the wild, would identify what species (or “one of those”) the creature belongs to, think about how that species of thing works, and try to have and use timeless and universal principles for dealing with it effectively.

Seeing events in this way helped shift my perspective from being caught in the blizzard of things coming at me to stepping above them to see their patterns through time.[2] The more related things I could understand in this way, the more I could see how they influence each other—e.g., how the economic cycle works with the political one—and how they interact over longer periods of time. I also learned that when I paid attention to the details I couldn’t see the big picture and when I paid attention to the big picture I couldn’t see the details. Yet in order to understand the patterns and the cause-effect relationships behind them, I needed to see with a higher-level, bigger-picture perspective and a lower-level, detailed perspective simultaneously, looking at the interrelationships between the most important forces over long periods of time. To me it appears that most things evolve upward (improve over time) with cycles around them, like an upward-pointing corkscrew:

For example, over time our living standards rise because we learn more, which leads to higher productivity, but we have ups and downs in the economy because we have debt cycles that drive actual economic activity up and down around that uptrend.

I believe that the reason people typically missthe big moments of evolution coming at them in life is that we each experience only tiny pieces of what’s happening. We are like ants preoccupied with our jobs of carrying crumbs in our minuscule lifetimes instead of having a broader perspective of the big-picture patterns and cycles, the important interrelated things driving them, and where we are within the cycles and what’s likely to transpire. From gaining this perspective, I’ve come to believe that there are only a limited number of personality types going down a limited number of paths that lead them to encounter a limited number of situations to produce only a limited number of stories that repeat over time.[3]

The only things that change are the clothes the characters are wearing and the technologies they’re using.

This Study & How I Came to Do It

One study lead to another that led me to do this study. More specifically:

- Studying money and credit cycles throughout history made me aware of the long-term debt cycle (which typically lasts about 50-100 years), which led me to view what is happening now in a very different way than if I hadn’t gained that perspective. For example, before interest rates hit 0% and central banks printed money and bought financial assets in response to the 2008-09 financial crisis I had studied that happening in the 1930s, which helped us navigate that crisis well. From that research, I also saw how and why these central bank actions pushed financial asset prices and the economy up, which widened the wealth gap and led to an era of populism and conflict. We are now seeing the same forces at play in the post-2009 period.

- In 2014, I wanted to forecast economic growth rates in a number of countries because they were relevant to our investment decisions. I used the same approach of studying many cases to find the drivers of growth and come up with timeless and universal indicators for anticipating countries’ growth rates over 10-year periods. Through this process, I developed a deeper understanding of why some countries did well and others did poorly. I combined these indicators into gauges and equations that we use to produce 10-year growth estimates across the 20 largest economies. Besides being helpful to us, I saw that this study could help economic policy makers because, by seeing these timeless and universal cause-effect relationships, they could know that if they changed X, it would have Y effect in the future. I also saw how these 10-year leading economic indicators (such as the quality of education and the level of indebtedness) were worsening for the US relative to big emerging countries such as China and India. This study is called “Productivity and Structural Reform: Why Countries Succeed and Fail, and What Should Be Done So Failing Countries Succeed.”

- Soon after the Trump election in 2016 and with increases in populism in developed countries becoming more apparent, I began a study of populism. That highlighted for me how gaps in wealth and values led to deep social and political conflicts in the 1930s that are similar to those that exist now. It also showed me how and why populists of the left and populists of the right were more nationalistic, militaristic, protectionist, and confrontational—and what such approaches led to. I saw how strong the conflict between the economic/political left and right could become and the strong impact this conflict has on economies, markets, wealth, and power, which gave me a better understanding of events that were and still are transpiring.

- From doing these studies, and from observing numerous things that were happening around me, I saw that America was experiencing very large gaps in people’s economic conditions that were obscured by looking only at economic averages. So I divided the economy into quintiles—i.e., looking at the top 20% of income earners, the next 20%, and so on down to the bottom 20%—and examined the conditions of these populations individually. This resulted in two studies. In “Our Biggest Economic, Social, and Political Issue: The Two Economies—The Top 40% and the Bottom 60%,” I saw the dramatic differences in conditions between the “haves” and the “have-nots,” which helped me understand the greater polarity and populism I saw emerging. Those findings, as well as the intimate contact my wife and I were having through her philanthropic work with the reality of wealth and opportunity gaps in Connecticut communities and their schools, led to the research that became my “Why and How Capitalism Needs to Be Reformed” study.

- At the same time, through my many years of international dealings in and research of other countries, I saw huge global economic and geopolitical shifts taking place, especially in China. I have been going to China a lot over the last 35 years and am lucky enough to have become well-acquainted with its top policy makers. This has helped me see up close how remarkable the advances in China have been and how excellent the capabilities and historical perspectives that were behind them are. These excellent capabilities and perspectives have led China to become an effective competitor with the US in production, trade, technology, geopolitics, and world capital markets.

By the way you can read these studies for free at www.economicprinciples.org.

So, what you are now reading came about because of my need to understand important things that are now happening that hadn’t happened in my lifetime but have happened many times before that. These things are the result of three big forces and the questions they prompt.

1) THE LONG-TERM MONEY AND DEBT CYCLE

At no point in our lifetimes have interest rates been so low or negative on so much debt as they are today. At the start of 2020, more than $10 trillion of debt was at negative interest rates and an unusually large amount of additional new debt will soon need to be sold to finance deficits. This is happening at the same time as huge pension and healthcare obligations are coming due. These circumstances raised some interesting questions for me. Naturally I wondered why anyone would want to hold debt yielding a negative interest rate and how much lower interest rates can be pushed. I also wondered what will happen to economies and markets when they can’t be pushed lower and how central banks could be stimulative when the next downturn inevitably came. Would central banks print a lot more currency, causing its value to go down? What would happen if the currency that the debt is denominated in goes down while interest rates are so low? These questions led me to ask what central banks will do if investors flee debt denominated in the world’s reserve currencies (i.e., the dollar, the euro, and the yen), which would be expected if the money that they are being paid back in is both depreciating in value and paying interest rates that are so low.

In case you don’t know, a reserve currency is a currency that is accepted around the world for transactions and savings. The country that gets to print the world’s primary currency (now the US) is in a very privileged and powerful position, and debt that is denominated in the world’s reserve currency (i.e., US dollar-denominated debt) is the most fundamental building block for the world’s capital markets and the world’s economies. It is also the case that all reserve currencies in the past have ceased to be reserve currencies, often coming to traumatic ends for the countries that enjoyed this special privilege. So I also began to wonder whether, when, and why the dollar will decline as the world’s leading reserve currency—and how that would change the world as we know it.

2) THE DOMESTIC WEALTH AND POWER CYCLE

Wealth, values, and political gaps are now larger than at any other time during my lifetime. By studying the 1930s and other prior eras when polarity was also high, I’ve learned that which side wins out (i.e., left or right) will have very big impacts on economies and markets. So naturally I wondered what these gaps will lead to in our time. My examinations of history have taught me that, as a principle, when wealth and values gaps are large and there is an economic downturn, it is likely that there will be lot of conflict about how to divide the pie. How will people and policy makers be with each other when the next economic downturn arrives? I am especially concerned because of the previously mentioned limitations on central banks’ abilities to cut interest adequately to stimulate the economy. In addition to these traditional tools being ineffective, printing money and buying financial assets (now called “quantitative easing”) also widen the wealth gap because buying financial assets pushes up their prices, which benefits the wealthy who hold more financial assets than the poor.

3) THE INTERNATIONAL WEALTH AND POWER CYCLE

For the first time in my lifetime, the United States is encountering a rival power. China has become a competitive power to the United States in a number of ways and is growing at a faster rate than the US. If trends continue, it will be stronger than the United States in most of the most important ways that an empire becomes dominant. (Or at the very least, it will become a worthy competitor.) I have seen both countries up close for most of my life, and I now see how conflict is increasing fast, especially in the areas of trade, technology, geopolitics, capital, and economic/political/social ideologies. I can’t help but wonder how these conflicts, and the changes in the world order that will result from them, will transpire in the years ahead and what effects that will have on us all.

The confluence of these three factors piques my curiosity and most draws my attention to similar periods such as the 1930-45 period and numerous others before that. More specifically, in 2008-09 like in 1929-32, there were serious debt and economic crises. In both cases, interest rates hit 0% which limited central banks’ ability to use interest rate cuts to stimulate the economy, so, in both cases, central banks printed a lot of money to buy financial assets which, in both cases, caused financial asset prices to rise and widened the wealth gap. In both periods, wide wealth and income gaps led to a high level of political polarization that took the form of greater populism and battles between ardent socialist-led populists of the left and ardent capitalist-led populists of the right. These domestic conflicts stewed while emerging powers (Germany and Japan in the 1930s) increasingly challenged the existing world power. And finally, just like today, the confluence of these factors meant that it was impossible to understand any one of them without also understanding the overlapping influences among them.

As I studied these factors, I knew that the short-term debt cycle was getting late and I knew that a downturn would eventually come. I did not expect the global pandemic to be what brought it about, though I did know that past pandemics and other acts of nature (like droughts and floods) have sometimes been important contributors to these seismic shifts.

To gain the perspective I needed about these factors and what their confluence might mean, I looked at the rises and declines of all the major empires and their currencies over the last 500 years, focusing most closely on the three biggest ones: the US empire and the US dollar which are most important now, the British Empire and the British pound which were most important before that, and the Dutch Empire and the Dutch guilder before that. I also focused less closely on the other six other significant, though less dominant, empires of Germany, France, Russia, Japan, China, and India. Of those six, I gave China the most attention and looked at its history back to the year 600 because 1) China was so important throughout history, it’s so important now, and it will likely be even more important in the future and 2) it provides many cases of dynasties rising and declining to look at to help me better understand the patterns and the forces behind them. In these cases, a clearer picture emerged of how other influences, most importantly technology and acts of nature, played significant roles. From examining all these cases across empires and across time, I saw that important empires typically lasted roughly 250 years, give or take 150 years, with big economic, debt, and political cycles within them lasting about 50-100 years. By studying how these rises and declines worked individually, I could see how they worked on average in an archetypical way, and then I could examine how they worked differently and why. Doing that taught me a lot. My challenge is in trying to convey it well.

Remember That What I Don’t Know Is Much Greater Than What I Know

In asking these questions, from the outset I felt like an ant trying to understand the universe. I had many more questions than answers, and I knew that I was delving into numerous areas that others have devoted their lives to studying. So I aggressively and humbly drew on knowledge of some remarkable scholars and practitioners, who each had in-depth perspectives on some piece of the puzzle, though none had the holistic understanding that I needed in order to adequately answer all my questions. In order to understand all the cause-effect relationships behind these cycles, I combined my triangulation with historians (who specialized in different parts of this big, complicated history) and policy makers (who had both practical experiences and historical perspectives) with an examination of statistics drawn out of ancient and contemporary archives by my excellent research team and by reading a number of superb books on history.

While I have learned an enormous amount that I will put to good use, I recognize that what I know is still only a tiny portion of what I’d like to know in order to be confident about my outlook for the future. Still, I also know from experience that if I waited to learn enough to be satisfied with my knowledge, I’d never be able to use or convey what I have learned. So please understand that while this study will provide you with my very top-down, big-picture perspective on what I’ve learned and my very low-confidence outlook for the future, you should approach my conclusions as theories rather than facts. But please keep in mind that even with all of this, I have been wrong more times than I can remember, which is why I value diversification of my bets above all else. So, whenever I provide you with what I think, as I’m doing in this study, please realize that I’m just doing the best I can to openly convey to you my thinking.

It’s up to you to assess for yourself what I’ve learned and do what you like with it.

How This Study Is Organized

As with all my studies, I will attempt to convey what I learned in both a very short, simple way and in a much longer, more comprehensive way. To do so, I wrote this book in two parts.

Part 1 summarizes all that I learned in one very simplified archetype of the rises and declines of empires, drawing from all my research of specific cases. In order to make the most important concepts easy to understand, I will write in the vernacular, favoring clarity over precision. As a result, some of my wording will be by and large accurate but not always precisely so. (I will also highlight key sentences in bold so that you can just read these and skip the rest to quickly get the big picture.) I will first distill my findings into an index of total power of empires, which provides an overview of the ebbs and flows of different powers, that is constituted from eight indexes of different types of power. Then I go into an explanation of these different types of power so you can understand how they work, and finally I discuss what I believe it all means for the future.

Part 2 shows all the individual cases in greater depth, sharing the same indices for all the major empires over the last 500 years. Providing the information this way allows you to getthe gist of how I believe these rises and declines work by reading Part 1 and then to choose whether or not to go into Part 2 to see these interesting cases individually, in relation to each other, and in relation to the template explained in Part 1. I suggest that you read both parts because I expect that you will find the grand story of the evolutions of these countries over the last 500 years in Part 2 fascinating. That story presents a sequential picture of the world’s evolution via the events that led the Dutch empire to rise and decline into the British empire, the British empire to rise and decline into the US empire, and the US empire to rise and enter its early decline into the rise of the Chinese empire. It also compares these three empires with those of Germany, France, Russia, Japan, China, and India. As you will see in the examinations of each of them, they all broadly followed the script, though not exactly. Additionally, I expect that you will find fascinating and invaluable the stories of the rises and declines of the Chinese dynasties since the year 600 just like I did. Studying the dynasties showed me what in China has been similar to the other rises and declines (which is most everything), helped me to see what was different (which is what makes China different from the West), and gave me an understanding of the perspectives of the Chinese leaders who all study these dynasties carefully for the lessons they provide.

Frankly, I don’t know how I’d be able to navigate what is happening now and what will be coming at us without having studied all this history. But before we get into these fascinating individual cases, let’s delve into the archetypical case.

IMPORTANT DISCLOSURES

Information contained herein is only current as of the printing date and is intended only to provide the observations and views of Bridgewater Associates, L.P. (“Bridgewater”) as of the date of writing unless otherwise indicated. Bridgewater has no obligation to provide recipients hereof with updates or changes to the information contained herein. Performance and markets may be higher or lower than what is shown herein and the information, assumptions and analysis that may be time sensitive in nature may have changed materially and may no longer represent the views of Bridgewater. Statements containing forward-looking views or expectations (or comparable language) are subject to a number of risks and uncertainties and are informational in nature. Actual performance could, and may have, differed materially from the information presented herein. Past performance is not indicative of future results.

Bridgewater research utilizes data and information from public, private and internal sources, including data from actual Bridgewater trades. Sources include, the Australian Bureau of Statistics, Barclays Capital Inc., Bloomberg Finance L.P., CBRE, Inc., CEIC Data Company Ltd., Consensus Economics Inc., Corelogic, Inc., CoStar Realty Information, Inc., CreditSights, Inc., Credit Market Analysis Ltd., Dealogic LLC, DTCC Data Repository (U.S.), LLC, Ecoanalitica, EPFR Global, Eurasia Group Ltd., European Money Markets Institute – EMMI, Factset Research Systems, Inc., The Financial Times Limited, GaveKal Research Ltd., Global Financial Data, Inc., Haver Analytics, Inc., The Investment Funds Institute of Canada, Intercontinental Exchange (ICE), International Energy Agency, Lombard Street Research, Markit Economics Limited, Mergent, Inc., Metals Focus Ltd, Moody’s Analytics, Inc., MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Refinitiv, Renwood Realtytrac, LLC, RP Data Ltd, Rystad Energy, Inc., S&P Global Market Intelligence Inc., Sentix Gmbh, Spears & Associates, Inc., State Street Bank and Trust Company, Sun Hung Kai Financial (UK), Tokyo Stock Exchange, United Nations, US Department of Commerce, Wind Information (Shanghai) Co Ltd, Wood Mackenzie Limited, World Bureau of Metal Statistics, and World Economic Forum. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

The views expressed herein are solely those of Bridgewater and are subject to change without notice. In some circumstances Bridgewater submits performance information to indices, such as Dow Jones Credit Suisse Hedge Fund index, which may be included in this material. You should assume that Bridgewater has a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Bridgewater’s employees may have long or short positions in and buy or sell securities or derivatives referred to in this material. Those responsible for preparing this material receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.

This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment or other advice.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical or illustrative information that have inherent limitations. Unlike an actual performance record, simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or over compensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate.

Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater ® Associates, LP.

©2020 Bridgewater Associates, LP. All rights reserved

[1] To be clear, while I am describing these cycles of the past, I’m not one of those people who believe that what happened in the past will necessarily continue into the future without understanding the cause-effect mechanics that drive changes. My objective above all else is to have you join with me in looking at the cause-effect relationships and then to use that understanding to explore what might be coming at us and agree on principles to handle it in the best possible way.

[1a] For example, I have followed this approach for debt cycles because I’ve had to navigate many of them over the last 50 years and they are the most important force driving big shifts in economies and markets. If you are interested in understanding my template for understanding big debt crises and seeing all the cases that made it up, you can get Principles for Navigating Big Debt Crisesin free digital form at https://ift.tt/1b2l0yu or in print form for sale in bookstores or online. It was that perspective that allowed Bridgewater to navigate the 2008 financial crisis well when others struggled. I’ve studied many big, important things (e.g., depressions, hyperinflation, wars, balance of payments crises, etc.) by following this approach, usually because I was compelled to understand unusual things that appeared to be germinating around me.

[2] I approach seeing just about everything this way. For example, in building and running my business, I had to understand the realities of how people think and learn principles for dealing with these realities well, which I did using this same approach. If you are interested in what I learned about such non-economic and non-market things, I conveyed it in my book Principles: Life and Work, which is free in an app called “Principles in Action” available on the Apple App Store or is for sale in the usual bookstores.

[3] In my book Principles: Life and Work, I shared my thinking about these different ways of thinking. I won’t describe them here but will direct you there should you be interested.

As explained in the Introduction, the world order is now rapidly shifting in important ways that have never happened in our lifetimes but have happened many times before in history. My objective is to show you those cases and the mechanics that drove them and, with that perspective, attempt to imagine the future.

What follows here is an ultra-distilled description of the dynamics that I saw in studying the rises and declines of the last three reserve currency empires (the Dutch, the British, and the American) and the six other significant empires (Germany, France, Russia, India, Japan, and China) over the last 500 years, as well as all of the major Chinese dynasties back to the Tang Dynasty around the year 600. The purpose of this chapter is simply to provide an archetype to use when looking at all the cycles, most importantly the one that we are now in. In studying these past cases, I saw clear patterns that occurred for logical reasons that I briefly summarize here and cover more completely in subsequent chapters of Part 1. While the focus of this chapter and this book are on those forces that affected the big cyclical swings in wealth and power, I also saw ripple-effect patterns in all dimensions of life including culture and the arts, social mores, and more, which I will touch on in Part 2. By going back and forth between this simple archetype and the cases shown in Part 2, we will see how the individual cases fit the archetype (which is essentially just the average of those cases) and how well the archetype describes the individual cases. Doing this, I hope, will help us better understand what is happening now.

I’m on a mission to figure out how the world works and to gain timeless and universal principles for dealing with it well. It’s both a passion and a necessity for me. While the curiosities and concerns that I described earlier pulled me into doing this study, the process of conducting it gave me a much greater understanding of the really big picture on how the world works than I expected to get, and I want to share it with you. It made much clearer to me how peoples and countries succeed and fail over long swaths of time, it revealed giant cycles behind these ups and downs that I never knew existed, and, most importantly, it helped me put into perspective where we now are.

Though the big-picture synthesis that I’m sharing in this chapter is my own, you should know that the theories I express in this book have been well-triangulated with other experts. About two years ago, when I felt that I needed to answer the questions I described in the Introduction, I decided to immerse myself in research with my research team, digging through archives, speaking with the world’s best scholars and practitioners who each had in-depth understandings of bits and pieces of the puzzle, reading relevant great books by insightful authors, and reflecting on the prior research I’ve done and the experiences that I have from investing globally for nearly 50 years.

Because I view this as an audacious, humbling, necessary, and fascinating undertaking, I am worried about missing important things and being wrong, so my process is iterative. I do my research, write it up, show it to the world’s best scholars and practitioners to stress test it, explore potential improvements, write it up again, stress test it again, and so on, until I get to the point of diminishing returns. This study is the product of that exercise. While I can’t be sure that I have the formula for what makes the world’s greatest empires and their markets rise and fall exactly right, I’m confident that I got it by-and-large right. I also know that what I learned is essential for me putting what is happening now in perspective and for imagining how to deal with important events that have never happened in my lifetime but have happened repeatedly throughout history.

I’m passing it along to you to take or leave as you like.

The Countries Shown in This Study Had the Most Wealth and Power

This is a study of how wealth and power have come and gone in the leading powers of the world. To be clear, while the leading powers covered in this study were the richest and most powerful, they weren’t necessarily the best-off countries for two reasons. First, while wealth and power are what most people want and will fight over most, some people and their countries don’t think that these things are the most important and wouldn’t think of fighting over them. For example, some believe that having peace and savoring life are more important than having a lot of wealth and power and wouldn’t think of fighting hard enough to gain enough of the wealth and power to make it into the group included in this study. (By the way, I think there is a lot to be said for putting peace and savoring life ahead of gaining wealth and power.) Second, this group of countries excludes what I will call the “boutique countries” (like Switzerland and Singapore) that score very high in wealth and living standards but aren’t large enough to become one of the biggest empires.

Throughout History Wealth Was Gained by Either Making It, Taking It from Others, or Finding It in the Ground

Let’s start with the big-picture basics. Throughout recorded history various forms of groups of people (e.g., tribes, kingdoms, countries) have gained wealth and power by building it themselves, taking it from others, or finding it in the ground. When they gathered more wealth and power than any other group, they became the world’s leading power, which allowed them to determine the world order. When they lost that wealth and power, which they all did, the world order changed in very big ways. That changed all aspects of life in profound ways. In this chapter we will describe how throughout time the same basic forces have ebbed and flowed in basically the same sorts of ways to cause these ups and downs in empires.

Human productivity is the most important force in causing the world’s total wealth, power, and living standards to rise over time. Productivity—i.e., the output per person, driven by learning, building, and inventiveness—has steadily improved over time because learning is gained more than lost. However, it has risen at different rates for different people, though always for the same reasons—because of the quality of people’s education, inventiveness, work ethic, and economic systems to turn ideas into output. These reasons are important for policy makers to understand in order to achieve the best possible outcomes for their countries, and for investors and companies to understand in order to determine where the best long-term investments are.

But while significant, these learnings and productivity improvements are evolutionary, so they are not what cause big shifts in who has what wealth and power. They are caused by a number of forces, most importantly money and credit cycles. I have identified 17 important forces in total that have explained almost all of these movements throughout time, which we will delve into in a moment. These big forces generally transpire in classic cycles that are mutually reinforcing in ways that tend to create a single very big cycle of ups and downs. This big archetypical cycle governs the rising and declining of empires and influences everything about them, including their currencies and markets (which I’m especially interested in). As with the archetypical debt cycle, which I outlined in Principles for Navigating Big Debt Crises, this big cycle represents the archetypical one that we can compare others to, including the one that we are now in. I believe that we need to understand this archetypical cycle in order to put where we are in perspective and attempt to squint into the future.

Of the 17 forces, the debt cycle, the money and credit cycle, the wealth gap cycle, and the global geopolitical cycle are most important to understand in order to put where we are in perspective. For reasons explained in this book, I believe that we are now seeing an archetypical big shift in relative wealth and power and the world order that will affect everyone in all countries in profound ways. This big wealth and power shift is not obvious because most people don’t have the patterns of history in their minds to see this one as “another one of those.” So in this first chapter, I will describe in a very brief way how I see the archetypical mechanics behind rises and declines of empires and their markets working. Then we will delve into the various factors happening in the various past cases.

To See the Big Picture, You Can’t Focus on the Details

While I will attempt to paint this big sweeping picture accurately, I can’t paint it in a precise way, and, in order for you to see it and understand it, you can’t try to do so in a precise way. That is because we are looking at evolution over long time frames. To see it, you will have to let go of the details. Of course, when the details are important, which they often are, I will go from the very big, imprecise picture to a more detailed one.

Looking at what happened in the past from this very big-picture perspective will radically alter how you see things. For example, because the span of time covered is so large, many of the most fundamental things that we take for granted and many of the terms we use to describe them did not exist over the full period of time. As a result, I will be imprecise in my wording so that I can convey the big picture without getting tripped up on what might seem to be big things but, in the scope of what we are looking at, are relative details.

For example, I wrestled with how much I should worry about the differences between countries, kingdoms, nations, states, tribes, empires, and dynasties. Nowadays we think mostly in terms of countries. However, countries as we know them didn’t come into existence until the 17th century, after Europe’s Thirty Years’ War. In other words, before then there were no countries—generally speaking, though not always, there were kingdoms instead. In some places, kingdoms still exist and can be confused with being countries, and some places are both. Generally speaking, though not always, kingdoms are small, countries are bigger, and empires are biggest (spreading beyond the kingdom or the country). The relationships between them are often not all that clear. The British Empire was mostly a kingdom that gradually evolved into a country and then an empire that extended way beyond England’s borders, so that its leaders controlled broad areas and many non-English peoples. It’s also the case that each of these types of singularly controlled entities—countries, kingdoms, tribes, empires, etc.—controls its population in different ways, which further confuses things for those who seek precision. For example, in some cases empires are areas that are occupied by a dominant power while in other cases empires are areas influenced by a dominant power that controls other areas through threats and rewards. The British Empire generally occupied the countries in its empire while the American Empire has controlled more via rewards and threats—though that is not entirely true, as at the time of this writing the US has military bases in 70 countries. So, though it is clear that there is an American Empire, it is less clear exactly what is in it. Anyway, you get my point—that trying to be precise can stand in the way of conveying the biggest, most important things. So in this chapter you are going to have to bear with my sweeping imprecisions. You will also understand why I will henceforth imprecisely call these entities countries, even though not all of them were countries, technically speaking.

Along these lines, some will argue that my comparing different countries with different systems in different times is impossible. While I can understand that perspective, I want to assure you that I will seek to explain whatever major differences exist, that the timeless and universal similarities are much greater than the differences, and that to let the differences stand in the way of seeing those similarities which provide us with the lessons of history we need, would be tragic.

Most Everything Evolves in an Uptrend with Cycles Around It

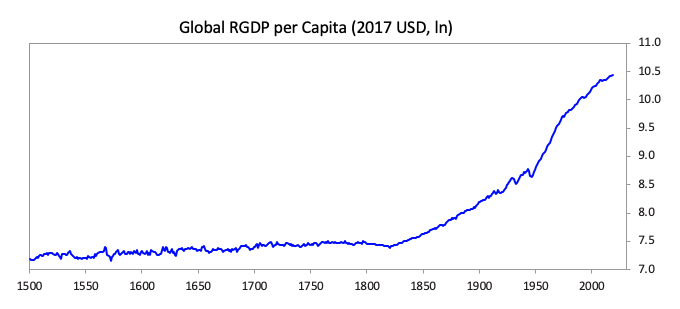

As mentioned earlier, over long periods of time we evolve because we learn to do things better, which raises our productivity. Over the long run, that is the most important force, though over the short run, the swings around this upward trend are most important. This is conveyed in the chart below, which shows the estimated output (i.e., estimated real GDP) per person over the last 500 years. As shown from this top-down, big-picture perspective, output per person appears to be steadily improving, though very slowly in the early years and faster after around 1800, when the slope up becomes much steeper, reflecting the faster productivity gains. This shift from slower productivity gains to faster productivity gains was primarily due to the improvements in broad learning and the conversion of that learning into productivity. That was brought about by a number of factors going as far back as the invention of the printing press in Europe in the mid-15th century (it had been used in China substantially earlier), which increased the knowledge and education available to many more people, contributing to the European Renaissance, the Scientific Revolution, the Enlightenment, and the first Industrial Revolution in Britain.

That broader-based learning also shifted wealth and power away from 1) an agriculture-based economy in which land ownership was the principal source of power, and the monarchies, nobles, and church worked together to maintain their grip on it, toward 2) an industrial-based economy in which inventive capitalists created and owned the means of production of industrial goods and worked together with those in government to maintain the system that allowed them to have the wealth and power. In other words, since the Industrial Revolution, which brought about that change, we have been operating in a system in which wealth and power have primarily come more from the combination of education, inventiveness, and capitalism, with those who run governments working with those who control most of the wealth and education. While in the first half of the 20th century there were deviations away from capitalism toward communism (which in the years between 1950 and 1990 showed that it didn’t work in the forms that have been tried) and socialism (which is essentially a hybrid wealth and opportunity distribution system that people can debate the merit of), the formula for success has been a system in which educated people come up with innovations, receive funding through capital markets, and own the means by which their innovations are turned into the production and allocation of resources, allowing them to be rewarded by profit-making. This happens best in capitalism and the government systems that work symbiotically with it. At the same time, how this is happening continues to evolve. For example, while ages ago agricultural land and agricultural production were worth the most and that evolved into machines and what they produced being worth the most, digital things that have no apparent physical existence (data and information processing) are evolving to become worth the most. That will create a fight over who obtains the data and how they use it to have wealth and power. (We will delve into that in the chapter that deals with learning and improving to raise productivity.) The main point I’m trying to get across is that the greatest power that produces these uptrends in living standards is humanity’s ability to adapt and improve—so much so that movements around that uptrend caused by everything else don’t even show up when one looks at what’s happening from the higher level in order to gain a bigger-picture perspective.

At the same time, like all such systems, capitalism has failed to do that job well enough to achieve the goals of producing equal opportunity and maximum productivity through broad-based human capital development (for more on that see “Why and How Capitalism Needs to Be Reformed”). But, to reiterate the main point: from the top-down, big-picture level shown in the below chart, things pretty much keep getting better because people keep getting smarter and keep conveying that smartness into more and better output.

Underneath this relatively smooth upward trajectory of learning and productivity are turbulent historical periods, including booms, busts, revolutions, and wars. History shows us that almost all of these turbulent times are due to money and credit collapses, big wealth gaps, fighting over wealth and power (i.e., revolutions and wars), and severe acts of nature (like droughts, floods, and epidemics). It also shows that how bad these periods get depends almost exclusively on how strong the countries are to endure them. For example, those with large savings, low debts, and a strong reserve currency can withstand economic and credit collapses better than those that don’t have much savings, have a lot of debt, and don’t have a strong reserve currency. Likewise those with strong and capable leadership and civil populations can be managed better than those that don’t have these, and those that are more inventive will adapt better than those that are less inventive. As you will read in the cases in Part 2, these factors are measurable timeless and universal truths.

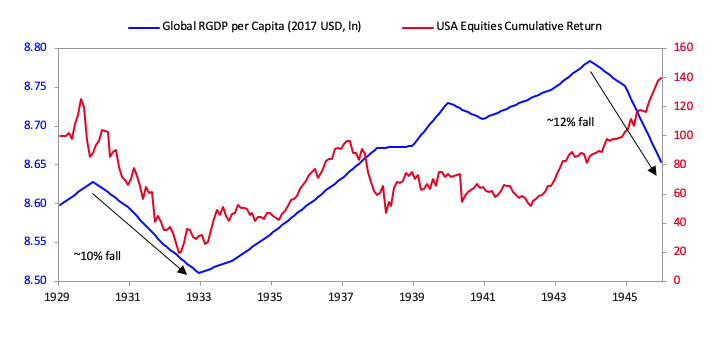

Because these turbulent times are small in relation to the evolutionary uptrend of humanity’s capacity to adapt and invent, they barely show up in the previous chart, appearing only as relatively minor wiggles. Yet these wiggles seem very big to us because we are so small and short-lived. Take the 1930-45 depression and war period, for example. The levels of the US stock market and global economic activity are shown in the chart below. As you can see, the economy fell by about 10%, and the stock market fell by about 85% and then began to recover.

This is part of the classic money and credit cycle that has happened for as long as there has been recorded history and that I will explain in the money and credit cycles chapter. More specifically, a credit collapse that happened because there was too much debt so the central government had to spend a lot of money it didn’t have and make it easier for debtors to pay their debt. To do that, the central bank had to print money and liberally provide credit—like they are doing now. When credit collapsed, spending collapsed with it so they had to print money. In that case the debt bust was the natural extension of the Roaring ‘20s boom that became a debt-financed bubble that popped in 1929. Almost all debt busts, including the one we are now in, come about for basically the same reason of extrapolating the uptrend forward and over-borrowing to bet heavily on things going up and being hurt when they go down.

Back then, the popping of the bubble and the resulting economic bust were the biggest influences on the 1930-45 period’s internal and external fight for wealth and power. Then, like now and like in most other cases, there were large wealth gaps, which when heightened by debt/economic collapses led to revolutionary changes in social and economic programs and big wealth transfers that were manifest in different systems in different places. Clashes and wars developed over which of these systems was best and as different people and countries fought to get their share. The popular systems that were fought over included communism (which supported dividing most wealth pretty much equally), fascism (which was autocratic state-controlled capitalism), and socialized democracy (which redistributed a lot of wealth while maintaining democracy and a more free-market capitalism—though often in a more autocratic form during the war years). There are always arguments or fights between those who want to make big redistributions of wealth and those who don’t. In the US in the 1930s, Mother Nature also gave us a painful drought.

Looking over the whole of the cases I examined, I’d say that past economic and market declines each lasted about three years until they were reversed through a big restructuring process that included restructuring of the debt and the monetary and credit system, fiscal policies of taxation and spending, and changes in political power. The quicker the printing of money to fill the debt holes, the quicker the closing of the deflationary depression and the sooner the worrying about the value of money begins. In the 1930s US case, the stock market and the economy bottomed the day that newly elected President Roosevelt announced that he would default on the government’s promise to let people turn in their money for gold, and that the government would create enough money and credit so that people could get their money out of banks and others could get money and credit to buy things and invest. As shown in the previous chart, that created a big improvement but not a full recovery. Then came the war, which resulted from fighting over wealth and power as the emerging powers of Germany and Japan challenged the existing leading world powers of Great Britain, France, and eventually the US (which was dragged into the war). The war period raised economic output of things that were used in war, but it would be a misnomer to call the war years a “productive period”—even though when measured in output per person, it was—because there was so much destruction. At the end of the war, global GDP per capita had fallen by about 12%, much of which was driven by declines in the economies of countries that lost the war. The stress test that these years represented wiped out a lot, made clear who the winners and losers were, and led to a new beginning and a new world order in 1945. Classically that was followed by a lengthy period of peace and prosperity that became overextended so that all countries are now, 75 years later, being stress tested again.

Most cycles in history happened for basically the same reasons. For example, the 1907-19 period began with the Panic of 1907, which, like the 1929-32 money and credit crisis following the Roaring ‘20s, was the result of boom periods (the Gilded Age in the US, the Belle Époque in continental Europe, and the Victorian era in Great Britain) becoming debt-financed bubbles that led to economic and market declines. These declines also happened when there were large wealth gaps that led to big wealth redistributions and a world war. The wealth redistributions, like those in the 1930-45 period, came about through large increases in taxes and government spending, big deficits, and big changes in monetary policies that monetized the deficits. Then Mother Nature brought about a pandemic (the Spanish flu) that intensified the stress test and the resulting restructuring process. This stress test and global economic and geopolitical restructuring led to a new world order in 1919, which was expressed in the Treaty of Versailles. That ushered in the 1920s debt-financed boom, which led to the 1930-45 period and the same things happening again.

Basically these periods of destruction/reconstruction cleaned out the weak, made clear who the powerful were, and established revolutionary new approaches to doing things that set the stage for periods of reconstruction and prosperity that became overextended as debt bubbles with large wealth gaps and led to debt busts that produced new stress tests and destruction/reconstruction periods, which eventually again led to the strong gaining relative to the weak, and so on.

What are these destruction/reconstruction periods like for the people who experience them? Since you haven’t been through one of these and the stories about them are very scary, the prospect of being in one is very scary to most people. It is true that these destruction/reconstruction periods have produced tremendous human suffering both financially and, more importantly, in lost or damaged human lives. Like the coronavirus experience, what each of these destruction/reconstruction periods has meant and will mean for each person depends on each person’s own experiences, with the broader deep destruction periods damaging the most people. While the consequences are worse for some people, virtually no one escapes the damage. Still, history has shown us that typically the majority of people stay employed in the depressions, are unharmed in the shooting wars, and survive the natural disasters.

Some people who struggled through them have even described these very difficult times as bringing about important, good things like drawing people closer together, building strength of character, learning to appreciate the basics, etc. For example, Tom Brokaw called the people who went through these times “the Greatest Generation” because of the strength of character it gave them. My parents and aunts and uncles who went through the Great Depression and World War II, as well as others of their era whom I’ve spoken to in other countries who went through their own versions of this destruction period, saw it that way too. Keep in mind that economic destruction periods and war periods typically don’t last very long—they tend to last roughly two or three years. And the lengths and severities of natural disasters (like droughts, floods, and epidemics) vary, though they typically lessen in painfulness as adaptations are made. One rarely gets all three of these types of big crises—i.e., 1) economic, 2) revolution and/or war, and 3) natural disaster—at the same time.

My point is that while these periods can be depressing and lead to a lot of human suffering, we should never, especially in the worst of times, lose sight of the fact that humanity’s power to adapt and quickly get to new, higher levels of well-being is much greater than all the bad stuff that can be thrown at us. For that reason, I believe that it is smart to believe and invest in humanity’s adaptability and inventiveness. So, while I am pretty sure that in the coming years both you and the world order will experience big challenges and changes, I believe that humanity will become smarter and stronger in very practical ways that will lead us to overcome these challenging times and go on to new and higher levels of prosperity.

Now let’s look at the cycles of rises and declines in the wealth and power of the major countries over the last 500 years.

The Shifts in Wealth and Power That Occurred Between Countries

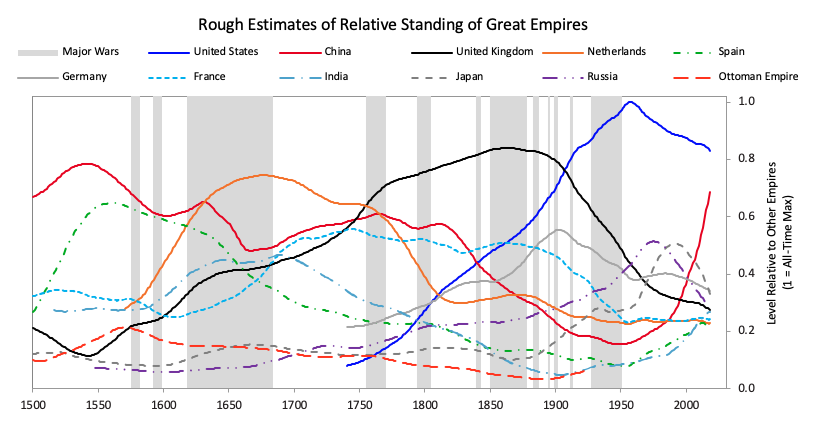

While the first chart of rising productivity shared previously was for the whole world (to the best of our ability to measure it), it doesn’t show the shifts in wealth and power that occurred between countries. The chart below shows you the relative wealth and power of the 11 leading empires over the last 500 years.1 Each one of these indices of wealth and power is a composite of eight different measures that I will explain shortly. Though these indices aren’t perfect because all data through time isn’t perfect, they do an excellent job of painting the big picture. As you can see, nearly all of these empires saw periods of ascendancy followed by periods of decline. The thicker lines represent the four most important empires: the Dutch, British, American, and Chinese. These empires held the last three reserve currencies—the US now, the British before it, and the Dutch before that. China is included because it has risen to be the second-most powerful empire/country and because it was so consistently powerful in most years prior to around 1850. To very briefly summarize what the chart shows:

- China was dominant for centuries (consistently outcompeting Europe in goods trade), though it entered a steep decline starting in the 1800s.

- The Netherlands, a relatively small country, became one of the world’s great empires in the 1600s.

- The UK followed a very similar path, peaking in the 1800s.

- Finally, the US rose to become the world’s superpower over the last 150 years, though particularly during and after WWII, and is now in relative decline while China is catching up once again.

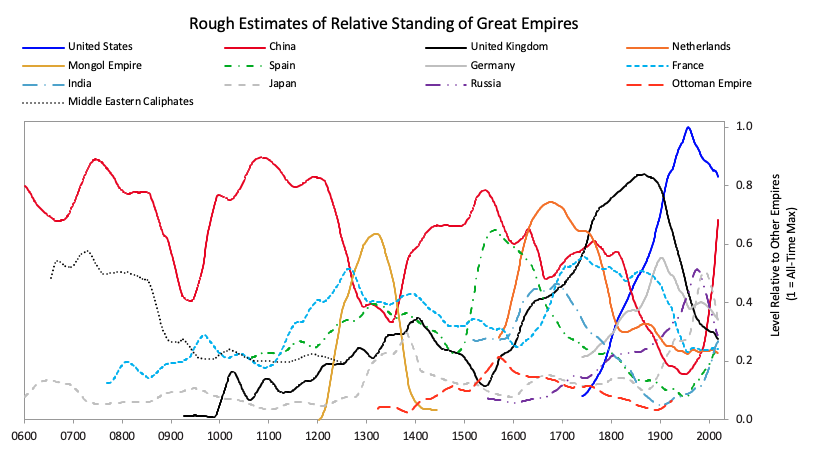

Now let’s look at the same chart that extends the data all the way back to the year 600. I focused on the one above (which covers just the last 500 years) rather than the one below (which covers the last 1,400 years) because it includes the empires I focused on most intently on and is simpler, though with 11 countries, 12 major wars, and over 500 years, it can hardly be called simple. Still, the one below is more extensive and worth glancing at. I left out the shading of the war periods to lessen the confusion. As shown, in the pre-1500 period, China was almost always the most powerful, though the Middle Eastern caliphates, the French, the Mongols, the Spanish, and the Ottomans were also in the picture.

Our Measures of Wealth and Power

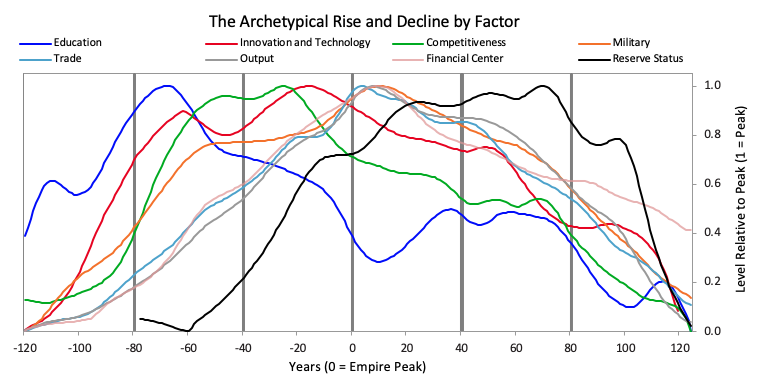

The single measure of wealth and power that I showed you for each country in the prior charts is made up as a roughly equal average of eight measures of strength. They are: 1) education, 2) competitiveness, 3) technology, 4) economic output, 5) share of world trade, 6) military strength, 7) financial center strength, and 8) reserve currency. While there are more measures of and influences on power that we will explore later, let’s begin by focusing on these key eight.

The chart below shows the average of each of these measures of strength, with most of the weight on the most recent three reserve countries (i.e., the US, the UK, and the Dutch).2

The lines on the chart do a pretty good job of telling the story of why and how the rises and declines took place. Using these and referring to some additional factors that we will delve deeper into later, I will describe that cycle in a nutshell. But before I start, it’s worth noting that all of these measures of strength rose and declined over the arc of the empire. That’s because these strengths and weaknesses are mutually reinforcing—i.e., strengths and weaknesses in education, competitiveness, economic output, share of world trade, etc., contribute to the others being strong or weak, for logical reasons. For example, it makes sense that better-educated people would produce societies that are more innovative, competitive, and productive. I call this cyclical interrelated move up and down “the Big Cycle.” Take note of the order that these items move up and down in the chart because it is broadly indicative of the processes that lead to the rising and declining of empires. For example, quality of education has been the long-leading strength of rises and declines in these measures of power, and the long-lagging strength has been the reserve currency. That is because strong education leads to strengths in most areas, including the creation of the world’s most common currency. That common currency, just like the world’s common language, tends to stay around because the habit of usage lasts longer than the strengths that made it so commonly used.

The Big Cycle

Broadly speaking, we can look at these rises and declines as happening in three phases: 1) the ascent phase, which is characterized by the gaining of competitive advantages; 2) the top phase, which is characterized by sustaining the strength but eventually sowing the seeds for the loss of the competitive advantages that were behind the ascent; and 3) the decline phase, which is characterized by self-reinforcing declines in all of these strengths.

In a nutshell, the ascent phase comes about when there is…

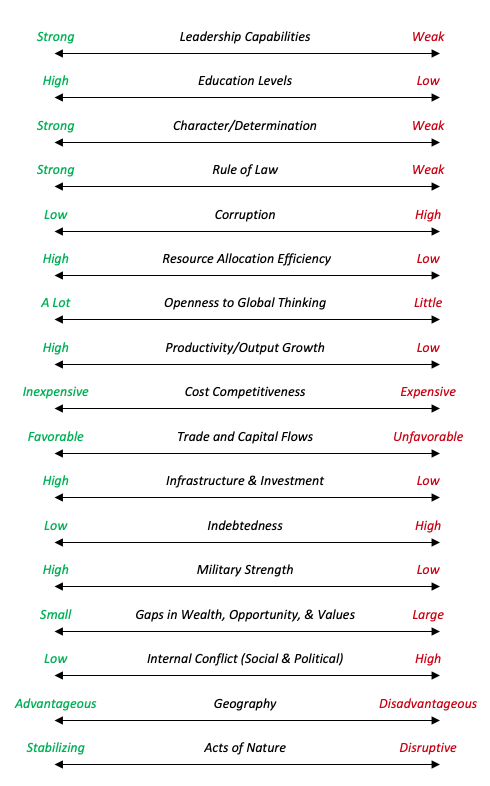

- strong enough and capable enough leadership to provide the essential ingredients for success, which include…

- strong education. By strong education I don’t just mean teaching knowledge and skills; I also mean teaching…

- strong character, civility, and a strong work ethic, which are typically taught in the family as well as in school. These lead to improved civility that is reflected in factors such as…

- low corruption and high respect for rules, such as rule of law.

- People being able to work well together, united behind a common view of how they should be together and a common purpose, is also important. When people have knowledge, skills, good character, and the civility to behave and work well together, and there is…

- a good system for allocating resources, which is significantly improved by…

- being open to the best global thinking, the country has the most important ingredients in order to succeed. That lead to them gaining…

- greater competitiveness in the global market, which brings in revenues that are greater than expenses, which leads them to have…

- strong income growth, which allows them to make…

- increased investments to improve their infrastructures, education systems, and research and development, which leads them to have…

- higher productivity (more valuable output per hour worked). Increasing productivity is what increases wealth and productive capabilities. When they achieve higher productivity levels, they can become productive inventors of…

- new technologies. These new technologies are valuable for both commerce and the military. As these countries become more competitive in these ways, naturally they gain…

- a significant share of world trade, which requires them to have…

- a strong military to protect their trade routes and to influence those who are important to it outside its borders. In becoming economically pre-eminent they develop the world’s leading…

- financial centers for attracting and distributing capital. (For example, Amsterdam was the world’s financial center when the Dutch empire was pre-eminent, London was it when the British empire was on top, and New York is now it because the US is on top, but China is beginning to develop its own financial center in Shanghai.) In expanding their trade globally, these growing empires bring their…

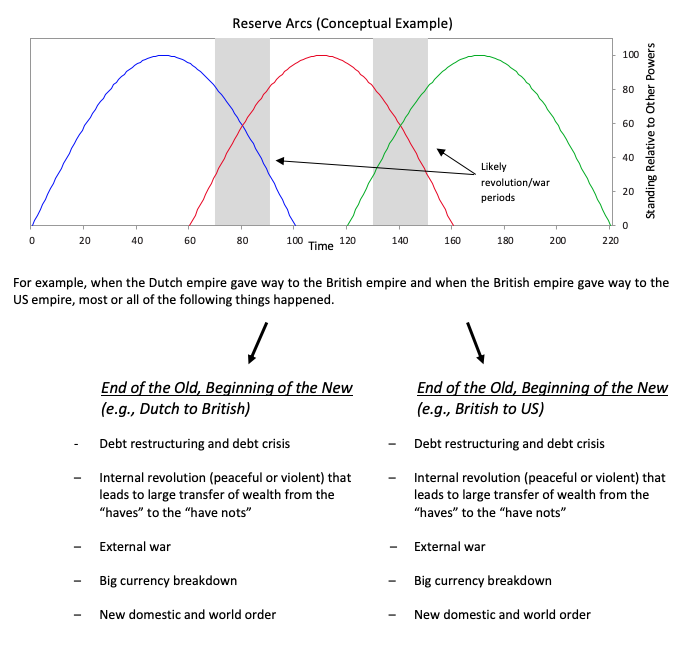

- strong equity, currency, and credit markets. Naturally those dominant in trade and capital flows have their currency used much more as the preferred global medium of exchange and the preferred storehold of wealth, which leads to their currency becoming a reserve currency. That is how the Dutch guilder became the world’s reserve currency when the Dutch Empire was pre-eminent, the British pound became the world’s reserve currency when the British Empire was pre-eminent, and the US dollar became the world’s reserve currency in 1944 when the US was about to win World War II and was clearly pre-eminent economically, financially, and militarily. Having one’s currency be a reserve currency naturally gives that country greater borrowing and purchasing power. As shown in the most recent chart, gaining and losing of reserve currency status happens with a significant lag to the other fundamentals.

It is through the mutually reinforcing and unwavering improvements in these things that countries rise and sustain their powers. Those who build empires allocate resources well by coordinating their economic, political, and military forces into a profitable economic/political/military system. For example, the Dutch created the Dutch East India Company, the British created the British East India Company, the US created the military-industrial complex, and China has Chinese state capitalism. Such economic, political, and military coordination has proved essential for all empires to profitably expand.

In a nutshell, the top phase typically occurs because within the successes behind the ascent lie the seeds of decline. More specifically, as a rule:

- Prosperous periods lead to people earning more, which naturally leads them to become more expensive, which naturally makes them less competitive relative to those in countries where people are willing to work for less.

- Those who are most successful typically have their ways of being more successful copied by emerging competitors, which also contributes to the leading power becoming less competitive. For example, British shipbuilders, who had less expensive workers than Dutch shipbuilders, hired Dutch shipbuilding architects to design ships that were built more cost-effectively than the Dutch ships. Because it takes less time and money to copy than invent, all else being equal, emerging empires tend to gain on mature empires through copying.

- Those who become richer naturally tend to work less hard, engage in more leisurely and less productive activities, and at the extreme, become decadent and unproductive. That is especially true as generations change from those who had to be strong and work hard to achieve success to those who inherited wealth—these younger generations tend to be less strong/battle-hardened, which makes them more vulnerable to challenges. Over time people in the prosperous society tend to want and need more luxuries and more leisure and tend to get weaker and more overextended in order to get them, which makes them more vulnerable.

- The currencies of countries that are richest and most powerful become the world’s reserve currencies, which gives them the “exorbitant privilege” of being able to borrow more money, which gets them deeper into debt. This boosts the leading empire’s spending power over the short term and weakens it over the longer run. In other words, when borrowing and spending are strong, the leading empire appears strong while its finances are in fact being weakened. That borrowing typically sustains its power beyond its fundamentals by financing both domestic over-consumption and the military and wars that are required to maintain its empire. This over-borrowing can go on for quite a while and even be self-reinforcing, because it strengthens the reserve currency, which raises the returns of foreign lenders who lend in it. When the richest get into debt by borrowing from the poorest, it is a very early sign of a relative wealth shift. For example, in the 1980s, when the US had a per capita income that was 40 times that of China’s, it started borrowing from Chinese who wanted to save in US dollars because the dollar was the world’s reserve currency. This was an early sign of that dynamic beginning. Similarly, the British borrowed a lot of money from its much poorer colonies, particularly during WWII, and the Dutch did the same before their top, which contributed to the reversals in their currencies and economies when the willingness to hold their currency and debt suddenly fell. The United States has certainly done a lot of borrowing and monetization of its debt, though this hasn’t yet caused a reduced demand for the US currency and debt.

- The leading country extends the empire to the point that the empire has become uneconomical to support and defend. As the costs of maintaining it become greater than the revenue it brings in, the unprofitability of the empire further weakens the leading country financially. That is certainly the case for the US.

- Economic success naturally leads to larger wealth gaps because those who produce a lot of wealth disproportionately benefit. Those with wealth and power (e.g., those who benefit commercially and those who run the government) naturally work in mutually supportive ways to maintain the existing system that benefits them while other segments of the population lag, until the split becomes so large that it is perceived as intolerably unfair. This is an issue in the US.

The decline phase typically happens as the excesses of the top phase are reversed in a mutually reinforcing set of declines, and because a competitive power gains relative strength in the previously described areas.

- When debts become very large, when the central banks lose their ability to stimulate debt and economic growth, and when there is an economic downturn, that leads to debt and economic problems and to more printing of money, which eventually devalues it.

- When wealth and values gaps get large and there is a lot of economic stress (wherever that stress comes from), there are high probabilities of greater conflict between the rich and the poor, at first gradually and then increasingly intensely. That combination of circumstances typically leads to increased political extremism—i.e., populism of both the left (i.e., those who seek to redistribute the wealth, such as socialists and communists) and the right (i.e., those who seek to maintain the wealth in the hands of the rich, such as the capitalists). That happens in both democratically and autocratically run countries. For example, in the 1930s, increasingly extreme populists of the left became communist and those from the right became fascist. Populists tend to be more autocratic, more inclined to fight, and more inclined to respect power than law.

- When the rich fear that their money will be taken away and/or that they will be treated with hostility, that leads them to move their money and themselves to places, assets, and/or currencies that they feel are safer. If allowed to continue, these movements reduce the tax and spending revenue in the locations experiencing these conflicts, which leads in turn to a classic self-reinforcing hollowing-out process in the places that money is leaving. That’s because less tax money worsens conditions, which raises tensions and taxes, causing still more emigration of the rich and even worse conditions, and so on. For example, we are now seeing some of that happening via the rich leaving higher-tax states where there is financial stress and large wealth gaps. When it gets bad enough, governments no longer allow that to happen—i.e., they outlaw the flows of money out of the places that are losing them and to the places, assets, and/or currencies that are getting them, which causes further panic by those seeking to protect themselves.

- When these sorts of disruptive conditions exist, they undermine productivity; that shrinks the economic pie and causes more conflict about how to divide the shrinking resources well, which leads to even more internal conflict that increasingly leads to fighting between the populist leaders from both sides who want to take control to bring about order. That is when democracy is most challenged by autocracy. This is why in the 1920s and 1930s Germany, Japan, Italy, and Spain (and a number of smaller countries) all turned away from democracy to autocratic leadership, and the major democracies (the US, the UK, and France) became more autocratic. It is widely believed that, during periods of chaos, more centralized and autocratic decision making is preferable to less centralized and more democratic, debate-based decision making, so this movement is not without merit when there is unruly, violent crowd fighting.

- When a country gains enough economic, geopolitical, and military power that it can challenge the existing dominant power, there are many areas of potential conflict between these rival world powers. Since there is no system for peacefully adjudicating such disputes, these conflicts are typically resolved through tests of power.

- When a leading country’s costs of maintaining its empire abroad become greater than the revenue that the empire brings in, that economically weakens the country. When that happens at the same time that other countries are emerging as rival powers, the leading power feels compelled to defend its interests. This is especially threatening to the leading country both economically and militarily, because greater military spending is required to maintain the empire, which comes when worsening domestic economic conditions are making it more difficult for leaders to tax and more necessary for them to spend on domestic supports. Seeing this dilemma, enemy countries are more inclined to mount a challenge. Then the leading power is faced with the difficult economic and military choice of fighting or retreating.

- When other exogenous shocks, such as acts of nature (e.g., plagues, droughts, or floods), occur during times of vulnerabilities such as those mentioned above, they increase the risk of a self-reinforcing downward spiral.

- When the leadership of the country is too weak to provide what the country needs to be successful at its stage in the cycle, that is also a problem. Of course, because each leader is responsible for leading during only a tiny portion of the cycle, they have to deal with, and can’t change, the condition of the country that they inherit. This means that destiny, more than the leader, is in control.