Many economic decisions are made after interpersonal persuasive communications, such as pitches to investors, sales presentations, and fundraiser events (McCloskey and Klamer 1995). In the economics literature, these interactions are often formalised by persuasion models (DellaVigna and Gentzkow 2010), which mostly focus on the content in persuasive interactions. The content may be informational, like the net present value (NPV) of a project and the key function of a new product (Stigler 1961). Conversely, the content may be noninformational, like the ‘framing’ (Mullainathan et al. 2008), the appealing peripheral content catering to people’s intuition and attracting attention (Bertrand et al. 2010), or the ‘models’ that lead receivers to interpret data and facts in a certain way (Schwartzstein and Sunderam 2020).

Beyond content, however, it is widely believed that the delivery in persuasive communications matters for the final outcome. Features like facial expression, tone of voice, or diction of speech can be impactful. These persuasion delivery features are dynamic and multi-dimensional and go beyond static traits of persuaders like how they look. As William Carlos Williams wrote, “It is not what you say that matters but the manner in which you say it...”

In a recent paper (Hu and Ma 2021), we study how venture capitalist make decisions in response to startup pitches. Venture capitalists are looking for firms that can grow, turn a profit, and eventually be sold or go public. They have to evaluate many factors, including the validity of a company’s business plan, the market fit, and the quality of the startup team. We show that investors can be unduly swayed when people pitching startup ideas appear enthusiastic, excited, and warm – even though these qualities revealed in the pitch do not lead to later success. The work may help unpack understudied channels through which persuasion affects economic decision making.

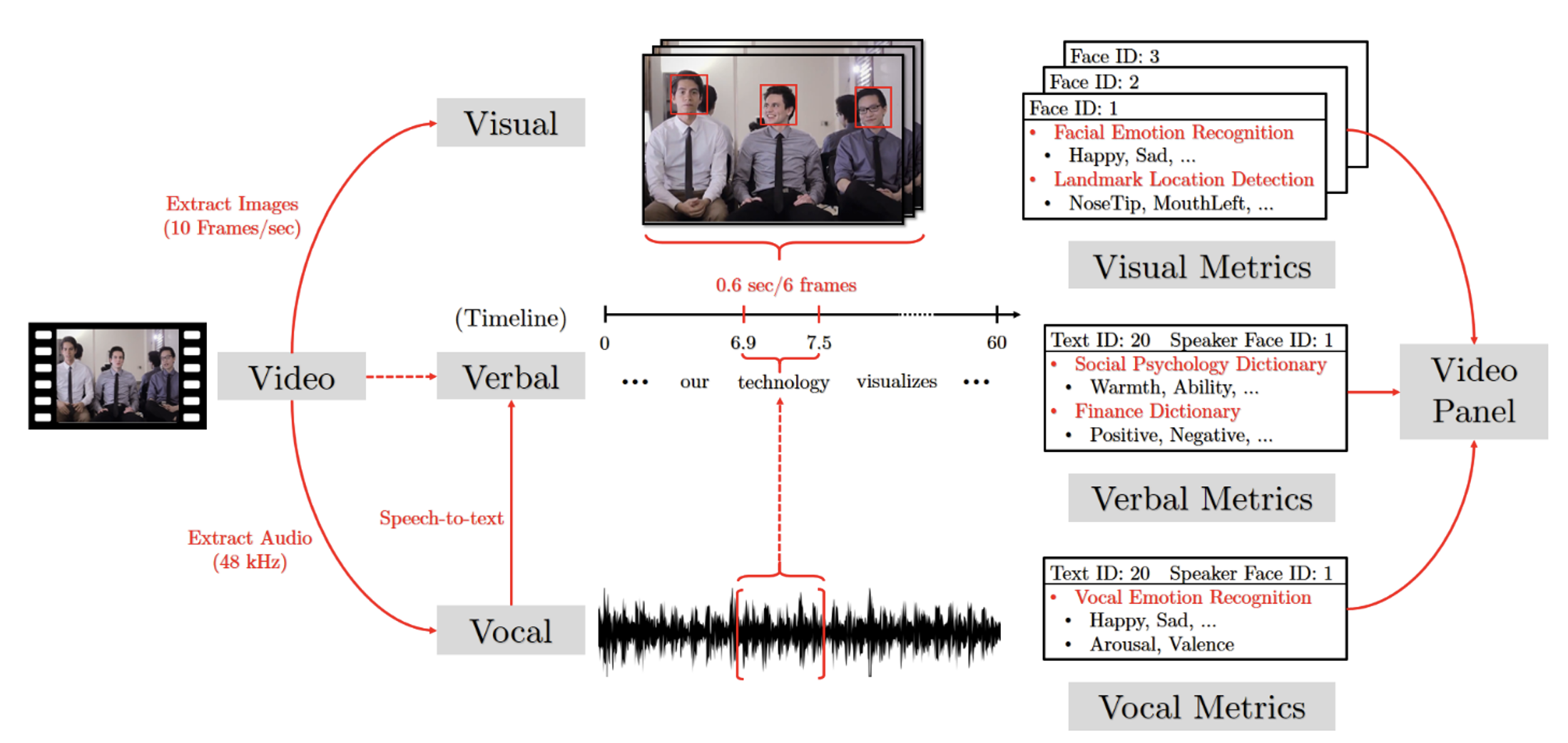

Quantifying the delivery of persuasion using videos and machine learning

To quantify the delivery of pitches, we collected more than 1,100 pitch videos that entrepreneurs submitted as part of their applications to a business accelerator. We then decompose each video into three streams of information:

- visual, consisting of a series of still images captured at a rate of 10 frames per second;

- vocal, consisting of the presentation’s audio; and

- verbal, consisting of the presentation’s transcript.

Using machine-learning algorithms from easily accessible computation services (such as Face++, Microsoft Azure, and Google Cloud), we then assess the level of enthusiasm present in each of these data streams. The algorithms generate detailed pitch features including visual emotions (e.g. positive, negative), vocal emotions (e.g. positive, negative, valence, arousal), textual sentiment (e.g. positive, negative), and psychological features (e.g. warmth). Based on those detailed features, we create an overall measure, the ‘pitch factor’, that summarises ‘how well’ the startup team delivers the pitch using a factor analysis. Empirically, the pitch factor loads positively on positivity dimensions and negatively on negativity dimensions, so intuitively the measure can be interpreted as the overall level of positivity – e.g. happiness, passion, warmth, enthusiasm – in a pitch.

This approach has two main advantages. First, our method captures dynamic and more complete information and across multiple information channels. Instead of focusing on static perceptions, we quantify the complete persuasion process across all three-V information dimensions through the whole pitch video. Second, our method has high scalability and replicability. Even though the underlying algorithms are trained and cross-checked using millions of subject-rated data points, our method does not involve subject recruiting. The algorithm can be viewed as a speedy, tireless, and well-trained rater following a consistent standard; thus, the method is replicable and ready to scale up computationally. This type of ML-based approach is increasingly useful in economic research. For example, Gorodnichenko et al. (2021) study the tone of voice in FOMC communications and its impacts on financial markets.

Figure 1 Illustration of the approach based on video data and machine learning

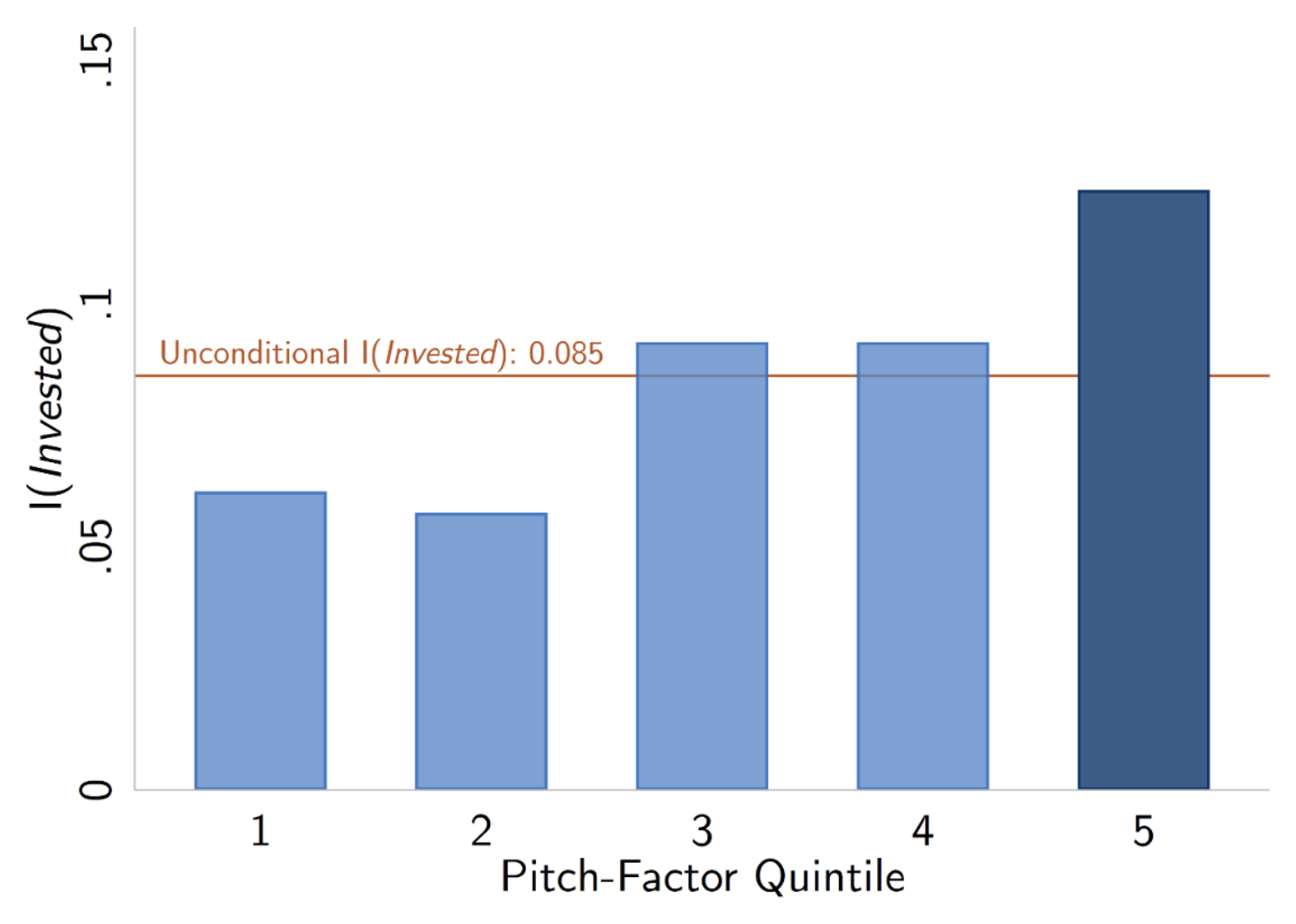

Does a passionate pitch matter? Yes!

Armed with the measures, we study how pitch delivery affects VC investment decisions. We find that teams that look more passionate and more positive are 17% more likely to receive funding; teams that sound more enthusiastic are 27% more likely to receive funding; and teams that use warmer and more engaging language are also more likely to be funded. (On the other hand, teams that discussed their own ability or competitiveness are penalized.) Overall, an above-average pitch factor increased the likelihood of investment by 35%.

Figure 2 Relationship between probability of receiving VC funding and overall positivity of pitch (‘pitch factor’)

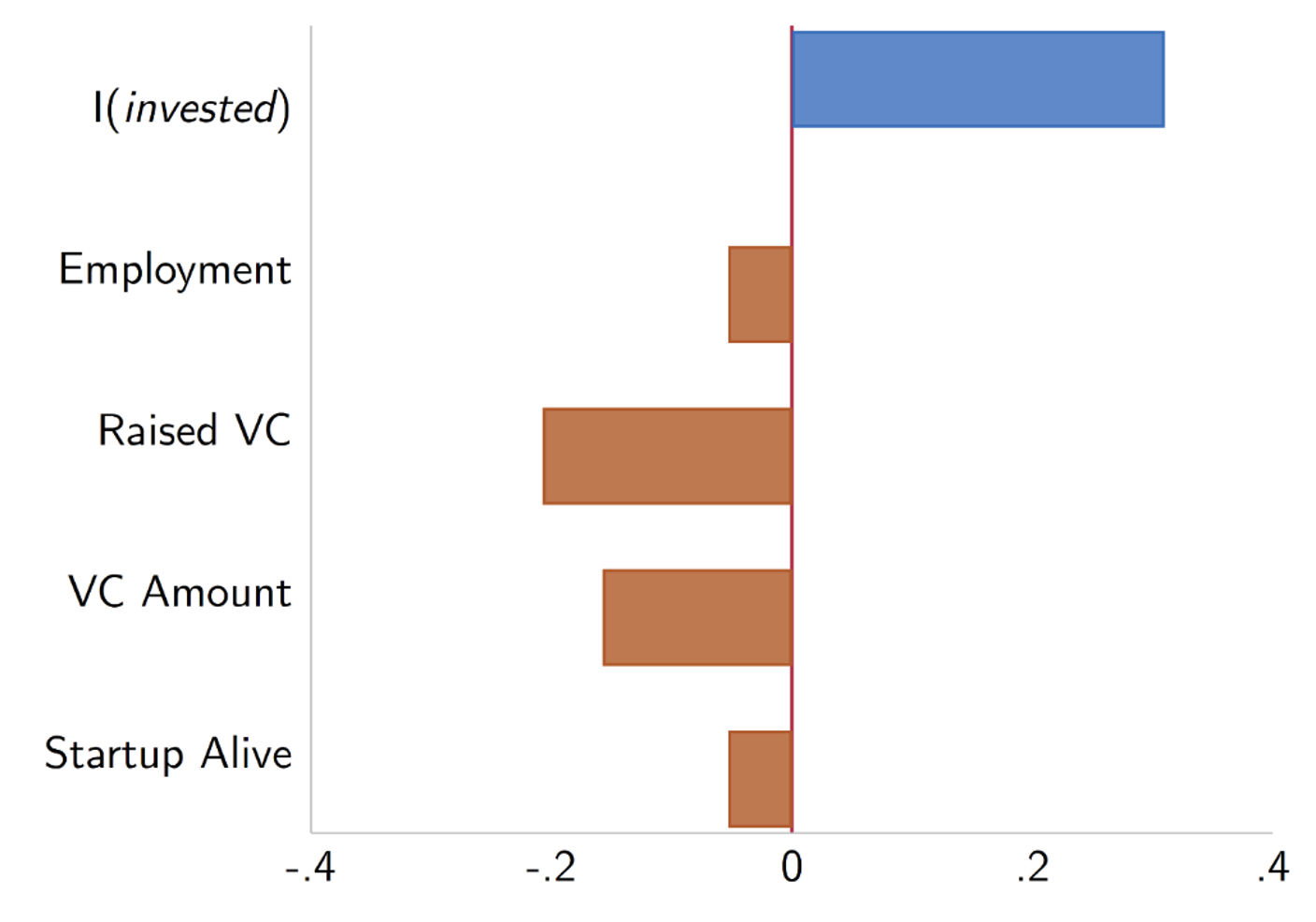

Is a passionate pitch a signal for future success?

Once they hit the market, though, these same firms underperformed, on average, based on key indicators like the total employment, the total amount of capital raised from VCs, whether they raised a second round of funding, and whether they stayed in business. Overall, startups with a high pitch factor underperform in the long run. In essence, an enthusiastic presentation overshadowed a lacklustre business plan. We do not interpret this as that the ability to deliver a passionate pitch is counterproductive. Instead, our preferred interpretation is that investors are too reluctant to invest in startups with a less positive pitch, and therefore only do so for the most promising companies, which in turn leads to better performance. In other words, a passionate pitch could lead investors to fund startups which may not merit the funding, suggesting a potential bias.

Figure 3 Relationship between ‘pitch factor’ and different outcomes

Heterogeneous effects across gender

The effect of pitch positivity was especially pronounced for teams composed entirely of women. In those cases, investment decisions were seven times more sensitive to the performance of the pitch. However, for teams comprising both genders, the performance of the male appeared to drive investment decisions, suggesting that women are simply ignored when they present alongside men. This result is consistent with the literature on gender stereotyping, which shows that women and men are evaluated differently in social interactions and economic decisions. Investors reward women who fit their stereotypes – that is, those whom they see as warmer and more positive – and aggressively avoid investing in women entrepreneurs who do not fit this profile. This effect connects to recent finding on the role of gender in startup financing (Ewens and Townsend 2020, Howell and Nanda 2020).

Why?

We explore two possible explanations for these results: taste-based channels (e.g. investors simply like to be around people who are positive) and inaccurate beliefs (e.g. investors incorrectly believe that more enthusiastic people actually have better ideas). We empirically test and separate these two mechanisms in a lab experiment. The experiment randomly allocates ten pitch videos to each subject to review and elicits subjects’ investment decisions and beliefs on firms’ long-term development. The results indicate that taste-based and belief-based channels both exist in this setting and contribute to the bias by 81.8% and 18.2%, respectively.

Implications for policy and practice

For entrepreneurs, the implications of these findings are obvious: remain as upbeat as possible in pitch meetings. For investors – and others who evaluate people based on how they present themselves and their work – our study sheds light on how to control for biases that slip below recognition. Our conclusions could be naturally extended to settings such as screening in the loan market and hiring in the labour market. In both cases, a diverse group of reviewers and the usage of consistent and robust machine learning-driven algorithms could possibly reduce bias induced by persuasive delivery.

References

Bertrand, M, D Karlan, DS Mullainathan, E Shafir and J Zinman (2010), “What's advertising content worth? Evidence from a consumer credit marketing field experiment”, Quarterly Journal of Economics 125(1): 263-306.

DellaVigna, S and M Gentzkow (2010), “Persuasion: empirical evidence”, Annual Review of Economics 2(1): 643-669.

Ewens, M and R R Townsend (2020), “Are early stage investors biased against women?”, Journal of Financial Economics 135(3): 653-677.

Gorodnichenko, Y, T Pham and O Talavera (2021), “The voice of monetary policy”, VoxEU.org, 25 April.

Howell, S and R Nanda (2020), “Networking frictions in venture capital and the gender gap in entrepreneurship”, VoxEU.org, 29 February.

Hu, A and S Ma (2021), “Persuading Investors: A Video-Based Study”, NBER Working Paper No. 29048.

McCloskey, D and A Klamer (1995), “One quarter of GDP is persuasion”, American Economic Review 85(2): 191-195.

Mullainathan, S, J Schwartzstein and A Shleifer (2008), “Coarse thinking and persuasion”, Quarterly Journal of Economics 123(2): 577-619.

Schwartzstein, J and A Sunderam (2021), “Using models to persuade”, American Economic Review 111(1): 276-323.

Stigler, G J (1961), “The economics of information”, Journal of Political Economy 69(3): 213-225.

from Hacker News https://ift.tt/2UBCeAR

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.