Over the last month both the algorithmic stablecoin Terra and its counterpart Luna fell to their demise. This has many in the cryptocurrency community searching for better algorithms and approaches.

While “stablecoins” as a construct are relatively new, the concept of pegging one currency to another is not. All historical approaches have failed when they reach a certain size. Notably:

-

The Bretton Woods system pegged currencies to the U.S. dollar (which was in turn pegged to gold). It collapsed in the 1970s.

-

George Soros famously “broke the Bank of England” when the pound sterling was forced to withdraw from the European Exchange Rate Mechanism.

-

China’s currency peg to the US Dollar has shifted to a “managed float” system.

We are able to prove from first principles that in the absence of outside funding algorithmic stablecoins cannot be stable. It is impossible to create a successful algorithm.

A special thanks to Vitalik Buterin. The ideas expressed in this proof were inspired by his recent fantastic thought experiments.

Proof

In order to assess the viability of an algorithmic stablecoin it’s helpful to break free from surrounding terminology and look at the economics of the construct. The proof below is algorithm-free and is thus universal.

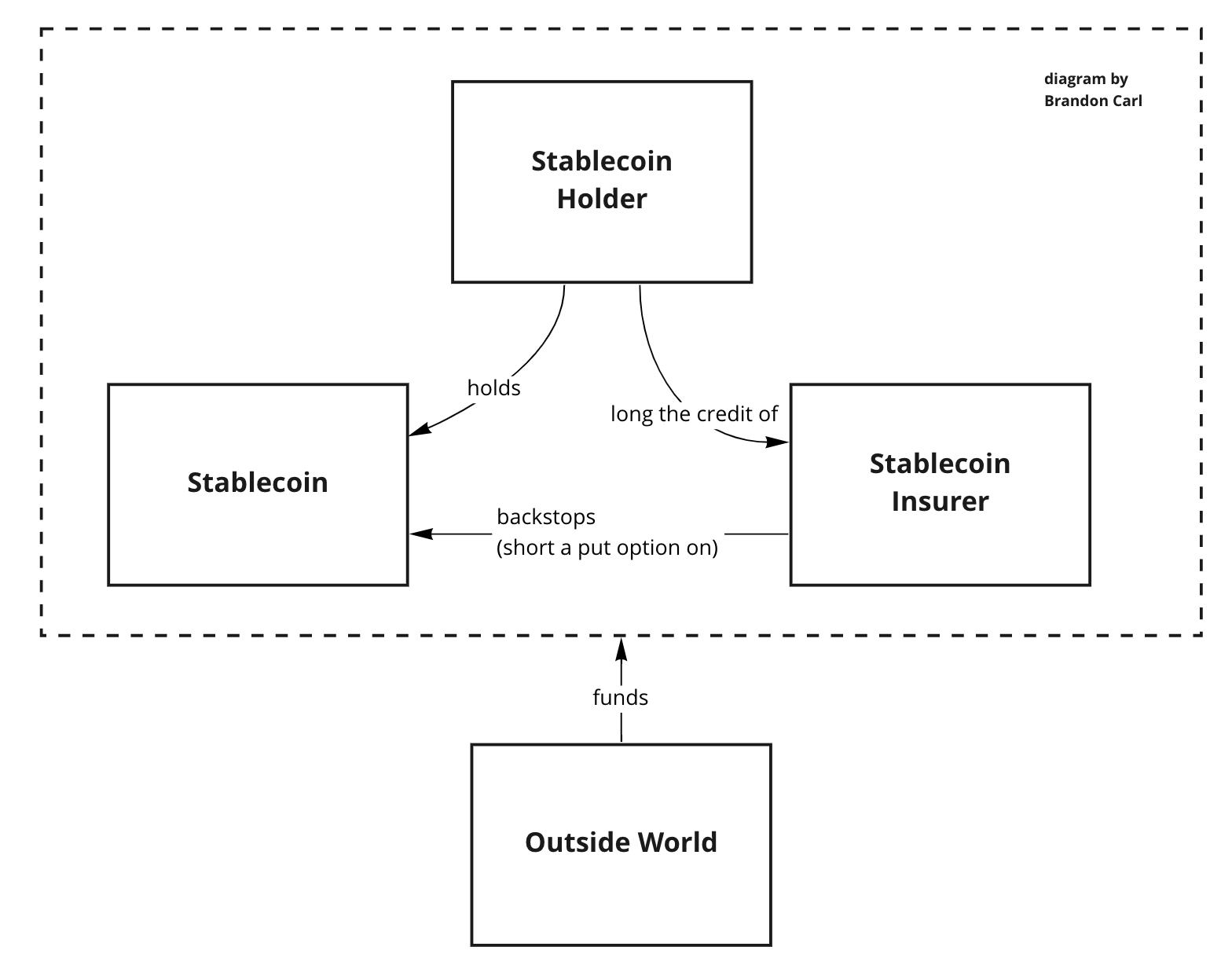

In our system there are three parties:

The fragility of the system becomes self-evident when we reframe the positions in terms of financial theory.

Stablecoin Insurers are short put options on the stablecoin.

In the event that the stablecoin falls, they must be able to cover the economic losses. This has two implications:

-

They must “delta hedge” their exposure in the event of a decline.

-

They should be compensated for the risk they assume. This is known as being “long theta” or “collecting decay” in financial options theory.

Stablecoin Holders are long the credit of the Stablecoin Insurers.

This is the equivalent of being short credit default swaps on the Stablecoin Insurers. As in Credit Default Swaps, they should be compensated for the risk they assume.

As a closed system this is inherently unstable.

Since both parties must be compensated for the risk they assume, neither party can make the other whole without assistance from the outside world:

-

In the event that the Stablecoin Holders compensate the Stablecoin Insurers, the value of their assets declines over time and is not stable.

-

In the event that the Stablecoin Insurers subsidize the Stablecoin Holders, they are not able to perform their job. Their “credit risk” once again destabilizes the system.

Continuous funding must come from the Outside World.

In the event that the funding comes from new entrants into the Stablecoin/Insurer ecosystem, the system is definitionally a Ponzi Scheme and is unstable.

To be in balance, the Stablecoin must provide real utility to the Outside World that transcends the Stablecoin/Insurer construct. Specifically:

-

There must be a transaction tax for real utility provided by the Stablecoin.

-

That transaction tax must be used to provide reserves for the Stablecoin. The amount of reserves required for the system to function (if it can) requires additional work.

-

If at any point in time the Stablecoin loses adoption, the transaction tax disappears and the system once again becomes unstable.

Real-World Application

If the above theory is correct, we should see theoretical price action play out in practice from a Terra and Luna postmortem.

Namely:

-

Luna should behave similar to a portfolio short put options. The value of the asset should have increased while Terra was stable (as they collect decay) and should decline sharply with a decline in Terra.

-

Terra should behave similar to a portfolio short credit default swaps. The value of the portfolio should stay relatively constant until the point as which the Luna Insurers creditworthy-ness becomes at risk.

Charts are courtesy of coinmarketcap.com

The Future

In order for us to make progress in innovation we must build our foundations on solid ground. Investments that are provably problematic should be appropriately regulated and efforts should be made to protect consumers against them. There are reports both of individuals losing everything in these “investments” and worse yet reports of suicide.

The findings above demonstrate without doubt that without continuous funding from the outside world algorithmic stablecoins are destined to fail. In the immediate, we must revise the haircuts and leverage on algorithmic stablecoins.

Let’s continue the outstanding innovation in the world of blockchain while simultaneously acknowledging the hard lessons learned and shifting focus to more fertile grounds.

Please reach out to me on LinkedIn or Twitter if you’d like to discuss further.

from Hacker News https://ift.tt/vwyAf2a

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.