Oil storage in Cushing, Okla.

Photographer: Johannes Eiele/AFP/ Getty Images

Photographer: Johannes Eiele/AFP/ Getty Images

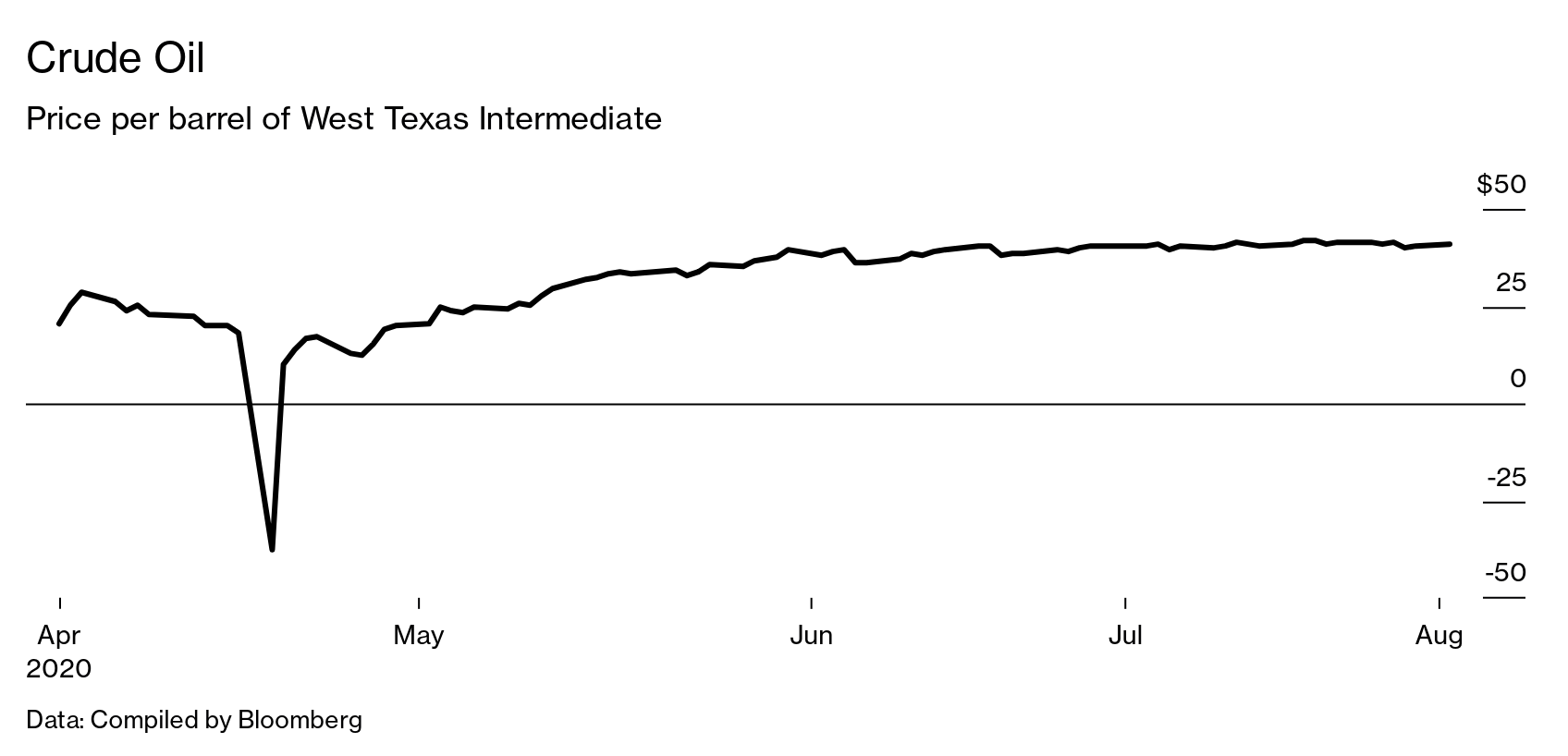

On April 20 the price of a barrel of oil for delivery the following month plummeted $40 in an hour, settling at –$37. It was the first time crude had ever crossed into negative territory. Regulators, oil executives, and investors have struggled to understand how a commodity at the heart of almost every aspect of global trade had fallen so far that sellers had to pay counterparties to take it off their hands.

But for a small group of veteran traders at a tiny London firm called Vega Capital London Ltd., the mystery mattered less than the results: They pocketed as much as $500 million that day, according to people familiar with the matter, who spoke to Bloomberg Businessweek on condition of anonymity.

Vega’s jackpot, which hasn’t been previously reported, involved about a dozen traders aggressively selling oil in unison before the May West Texas Intermediate contract settled at 2:30 p.m. in New York, the people say. It’s a tactic Vega’s traders used regularly, according to another person familiar with the firm’s strategy, but that day its trading coincided with a period of unprecedented volatility, when demand for fuel was wiped out by the coronavirus pandemic, and storage space in Cushing, Okla., where buyers take physical delivery of WTI crude, had all but disappeared.

Crude Oil

Price per barrel of West Texas Intermediate

Data: Compiled by Bloomberg

Now regulators at the U.S. Commodity Futures Trading Commission, the U.K.’s Financial Conduct Authority, and CME Group Inc., owner of the Nymex exchange where the trading took place, are examining whether Vega’s actions may have breached rules on trading around settlement periods and contributed to oil’s precipitous fall, according to people with knowledge of the probes.

Within 24 hours of the crash, the May WTI contract had bounced back to about $10 a barrel. And oil futures prices have continued to climb, with the active contract trading as high as $42.08 a barrel on August 4. But the plunge, however brief, created some big losers. They include thousands of Chinese and American retail investors who, lured by oil’s recent slump, had piled into instruments whose value was pegged to the contract’s April 20 settlement price.

Whether Vega’s windfall was a result of savvy trading, blind luck, or something else, the idea that a relative minnow could have such a profound impact calls into question CME Chief Executive Officer Terry Duffy’s April 22 declaration that the futures market had “worked to perfection.”

“The idea that the anomalies that day were a function solely of supply and demand is fanciful at best,” says Joe Cisewski, special counsel to Better Markets, a lobbying group that advocates for tougher regulation. “Oil producers, brokers, and other market participants have been sent into serious financial distress. Regulators need to objectively and thoroughly investigate what happened.”

Spokespeople for the CFTC, FCA, and CME declined to comment. The CFTC has said it’s looking to release a report on the crash later this year. Vega didn’t return emails seeking comment.

Prop-trading firms like Vega give independent traders access to the world’s exchanges, back-office services, and extra capital to trade with in exchange for a desk fee, a commission on every trade, and sometimes a share of any profits. In a trillion-dollar energy ecosystem dominated by the likes of BP, Glencore, and Royal Dutch Shell, prop firms are bit players.

Vega was started in 2016 by Adrian Spires and Tommy Gaunt, friends who’d worked together on the management team at another London prop firm, Tower Trading Group, before branching out on their own. In 2017 about 20 of Tower’s energy traders quit to join Vega, sparking a legal dispute that was settled out of court. Gaunt quit as a director last year, and Spires, 44, now owns all of the business. He left school at 18 to take a job in the trading pits of the London International Financial Futures and Options Exchange. Some of Vega’s traders spent time at the International Petroleum Exchange, buying and selling barrels of oil using hand signals, before commodities trading migrated from open outcry onto screens.

The firm has an office a short walk from Liverpool Street station, above one of London’s All Bar One pubs, which it shares with a group of mostly recent college graduates trading cryptocurrencies for another company also owned by Spires. But most of Vega’s traders work from home, according to people familiar with the firm, even more so since the U.K.’s lockdown came into force.

While more than two dozen individuals trade through Vega’s omnibus account, finding information about them is difficult. Only a few list Vega as their employer on LinkedIn. The company’s website has remained under construction since Vega was founded.

One oil investor describes the firm as something of a throwback to the days of the pits, when rowdy so-called locals made or lost fortunes before heading to the pub to celebrate their winnings or drown their sorrows. Many of Vega’s traders know each other socially, playing golf and taking ski trips. They also trade together during key periods to maximize their impact on the market, the people familiar with the firm say.

To understand how Vega wound up making so much money that day, it’s helpful to consider some of the idiosyncrasies of the oil market. Among the most popular ways to trade oil is Nymex’s WTI futures contract, which allows buyers and sellers to agree on a price for 1,000 barrels of light sweet crude for delivery at a future date. New contracts are released every month, and they settle at 2:30 p.m. on or near the 20th of the month.

Nymex also offers a corollary instrument called Trading at Settlement, or TAS, in which buyers and sellers agree to transact at whatever the settlement price turns out to be. The settlement price is based on a volume-weighted average of trades occurring in the two minutes before 2:30 p.m. While it might seem curious that anyone would agree to buy something without knowing the price, the TAS market is popular among exchange-traded funds and other funds whose mandate is to track the price of oil rather than to get the best deal. It was also central to Vega’s strategy.

One of the quirks of the oil futures market is that to take a long-term position, investors must keep buying new monthly contracts, then sell them before they expire and buy future months’ contracts, a process known as rolling. A significant proportion of the market’s participants are speculators with no interest in taking possession of any oil, so before each contract expires they have to close out any residual positions, creating a flurry of buying and selling.

In the lead-up to the April 20 settlement, rumors were circulating that there would be significant downward pressure on the May contract. The recent slump in prices had attracted bargain-hunting retail investors into funds that track oil, including the Bank of China Ltd.’s Treasure, a vehicle linked to the price of oil. To manage its position after the influx, Bank of China and the banks it uses to help execute trades needed to sell large numbers of the May contracts and buy June ones. Two weeks before the settlement, CME, which monitors market activity, issued a rare public warning that negative prices were a possibility.

On April 20, as Bank of China and others were selling May contracts, Vega’s traders were hoovering them up in the TAS market, according to people familiar with the matter, agreeing to buy oil at whatever the settlement price turned out to be. Then, as the settlement time approached, they aggressively sold outright WTI contracts and other related instruments, contributing to the downward pressure on the price. Vega stood to profit if it managed to buy oil through the TAS market more cheaply than the oil it sold through the day.

Vega’s selling collided with an exodus of buyers, and the May contract tumbled from about $10 at noon to zero at 2 p.m., then all the way down to settle at –$37. Oil’s dive into negative territory meant that Vega ended up being paid for many of the contracts it sold as the market was falling—and for all those it bought at the –$37 settlement price via TAS, locking in a huge profit.

Buying TAS and selling outrights before and during the settlement is a well-known strategy that dates back to the pits, according to market participants, but it carries considerable risk. Selling futures can quickly turn into losses if a bigger player shows up and starts buying. “It’s a big poker game,” says Greg Newman, founder of energy-trading firm Onyx Capital Group.

There are also rules that forbid trading with the goal of deliberately affecting the settlement. In 2008, Dutch firm Optiver was sanctioned by the CFTC for abusing the TAS mechanism and boasting about its exploits in emails. And in 2011 the agency introduced a rule prohibiting a practice known as “banging the close,” which it defines as trading heavily during the settlement period in one market to influence a larger position elsewhere.

But proving manipulation requires the government to demonstrate intent, which is difficult without incriminating communications such as text messages. And winning cases has been difficult, even with the new rules. “They’re not in any way slam-dunks,” says Aitan Goelman, a former head of the CFTC’s enforcement division and now a partner at Zuckerman Spaeder.

It seems unlikely that Vega’s traders could have predicted just how far oil would fall on April 20. Its selling that day met a whirlwind of other factors that spooked potential buyers and exaggerated all participants’ impact on the market. As a result, Vega’s traders made more money than they could have dreamed of—and found themselves in the authorities’ spotlight. That may explain why its traders, usually active on settlement days, weren’t active in May, June, and July, according to a person familiar with the firm’s trading. —With Jack Farchy

Read next: When Tesla Hits the S&P 500, It’ll Spark the Wildest Passive Trade Ever

(Updates with oil futures pricing. A previous update corrected “buyers” to “sellers” in first paragraph)

from Hacker News https://ift.tt/2D7vxxN

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.