Author's Note

1. Sorry for the delay in the newsletter. A busy week at work meant I could start writing this only on Sunday

2. Based on feedback, we introduced two features - "Read time" and "More reads on the topic"

3. Also, I understand many of you might be already aware of how Venture Capital works. Please feel free to jump out of this introductory piece :)

In 1940, Harvard Business School professor Georges Doriot, was drafted into the US Army for World War II. Once the war was over, he had different plans than teaching at Harvard. War had taught him the important role of science and technology in a country's progress. And he decided to pursue a new path. He set up the American Research & Development Corporation (ARDC) to facilitate the investment of private money into businesses started by soldiers. He raised money from sources other than wealthy families (very different from the norm then) with the aim to "encourage commercialization of technological innovations".

In 1957, ARDC invested $70,000 in a new company DEC that planned to make smaller and more affordable computers compared to what IBM was offering in the market at that point in time. 11 years later, in 1968, DEC IPO-ed valuing ARDC's share at $35M. ARDC had just made a cool 500x return and set the modern venture capital industry ablaze, interestingly in East Coast Boston.

But exactly in 1968, 3000 miles away in West Coast Silicon Valley, Robert (Bob) Noyce, a brilliant engineer, was readying to start a new company. He reached out to his friend Arthur Rock, who ran an investment firm, for money. Arthur put in $10,000 of his own and convinced his contacts to put in another $2.5M in practically 2 hours. Bob Noyce named his company Integrated Electronics, as in, Intel. The company went public 3 years later and Arthur would get back $8.2M - a 130% return or 33% annual return. 10 years later, Arthur would make a similar bet on Apple and net a 23,000% return!

Intel's deal would shift the center of venture capital investments to Silicon Valley, even before Boston could start making its name. Okay, enough of the origin story.

So...What is Venture Capital?

From the stories above, you must already have a guess. Venture capital is the investments of private capital in private companies, ie, companies not listed on the stock exchange.

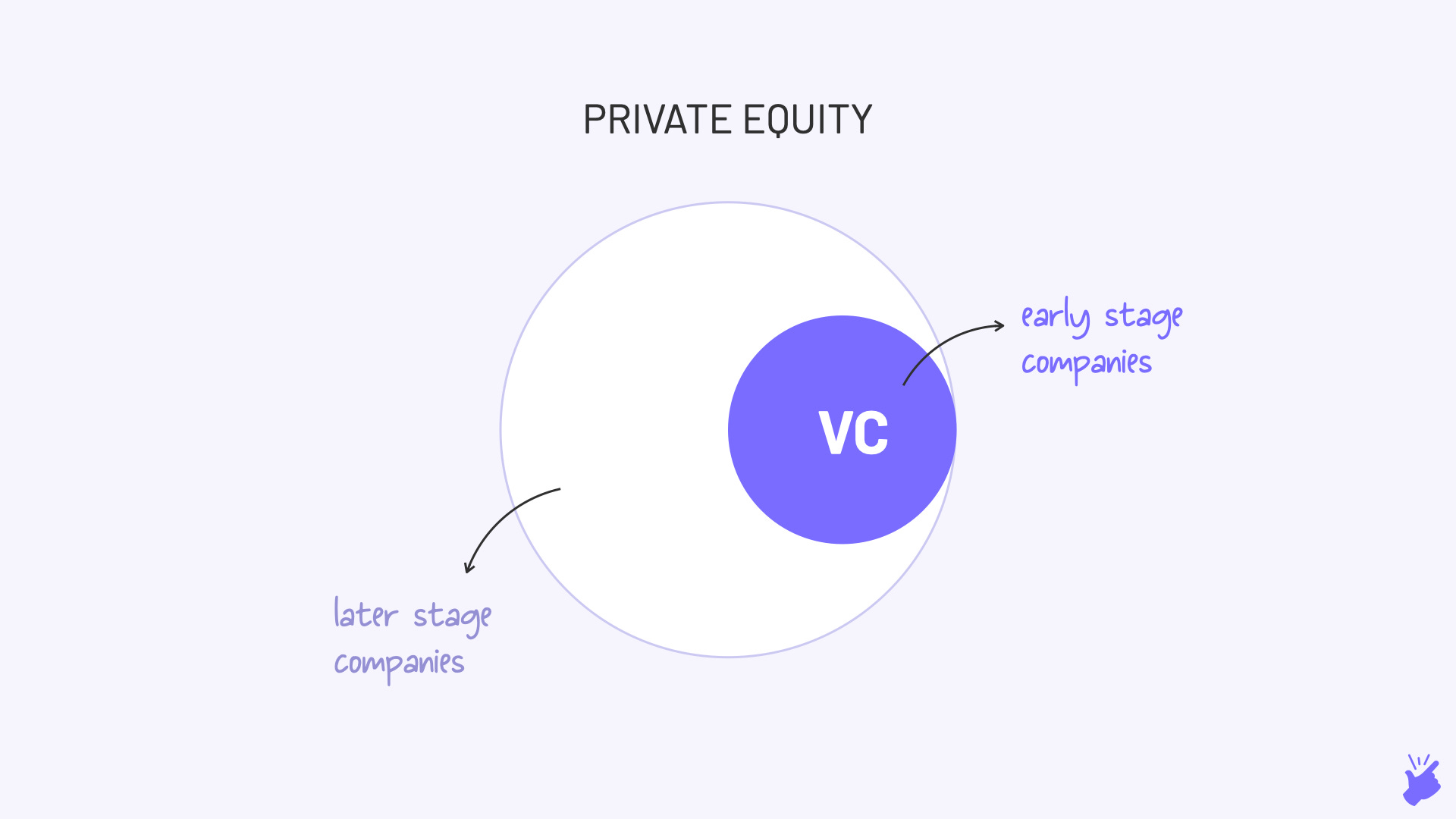

It is like Private Equity (PE) but a bit different. Venture capital focuses on companies very early in their lifecycle while PE invests in slightly more late-stage companies. It's this focus on early-stage companies (more risk) that puts the 'venture' in VC. But you will be right in saying VC is essentially a subset of PE.

Why does VC exist?

It exists because of the gaps in bank lending. Generally, if you wanted to start a new business, you would go to a bank. But banks lend only to new businesses that have hard assets against which they can secure the loan (eg, a factory). But in today's tech economy, many startups have few hard assets making a bank loan difficult for them.

Also, the risk of new businesses is very high. So high that even if banks are ready to lend, they have to charge such high interest rates that no one will take the loan.

The high-risk game that banks shy away from is where VC thrives. They are ready to give money to extremely young companies with no assets and probably inexperienced entrepreneurs as well. And for taking that risk, they take part ownership of the company instead of giving a loan. So they can capture more of the upside, meaning, they can take a share of the future profits.

Another difference is that bank = just money. But VC = money + advice on how to build businesses which is more useful to entrepreneurs.

How does VC work?

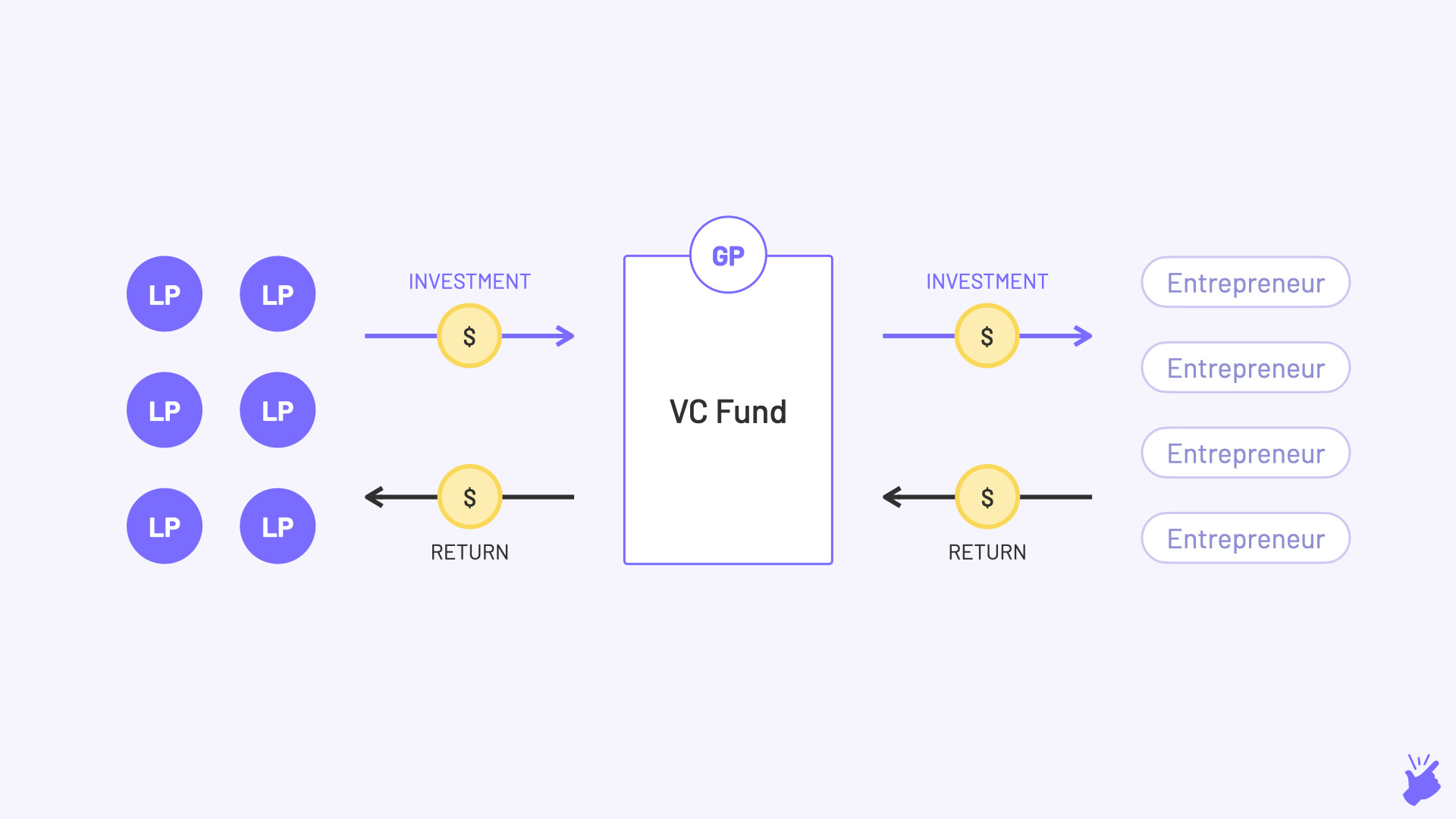

Limited partners

They are wealthy families, pension funds, insurance companies, and other such institutions who have large amounts of cash lying with them. They provide the money to the Venture Capital firm which in-turn invests in startups. But they don't run the VC firm (hence the term 'limited').

They are ready to invest in a VC fund because of the high returns expected from it compared to other options they have (public equity markets, debt, real estate, etc). But they also understand that it is an extremely risky investment and allocate only a small percentage of their cash to VC (generally 5-10%).

General Partners

They are generally investment professionals with proven track records who actually run the fund. And they have to balance multiple jobs:

-

Fundraise: They reach out to LPs and pitch the fund idea to them (they also actually make a deck like startup founders do). And hopefully collect cheques from them.

-

Invest: They have to discover startups (VCs call it "Deal Flow"), evaluate them ("Due Diligence") and then invest in them (write the cheque, duh!)

-

Grow: Now that they have invested in these startups, they help them grow by providing whatever help they can. It could be strategy, sourcing talent, introductions to potential partners, and even investors for the next fundraise.

-

Exit: The GPs either try to take the company public (IPO) or sell it to another company (M&A) or sell it to another investor (Secondary sale). This is the step where they make money and then return it to LPs

Fund Terms & Structure

Let's view this through an example. Introducing Bala. Bala is an investment professional and thinks there is potential to build huge businesses in India. So he wants to start a fund that can invest in and help build such businesses. Bala (the GP) now has to arrange for money from LPs, because well, he doesn't have any. So what are the details he will have to layout for an LP?

-

Fund Size

What is the amount Bala is planning to raise? $10M or $100M. Or $100B if Bala is like Masayoshi Son. -

Fund Theme

The areas that Bala will focus on-

What are the sectors he'll be investing in (Healthcare, Direct-to-consumer brands, etc)

-

Which stage of the company? (Seed, Series A...)

-

Which geographies? (India, South-east Asia...)

-

-

Hurdle Rate

This is the minimum yearly return (calculated as IRR) that Bala has to promise to generate for LPs. A failure to hit this rate means the fund has failed (and a lot of VC funds fail). Bala builds a financial model in Excel to calculate expected returns and figure out this hurdle rate. The sectors in focus and stage of investment will influence the hurdle rate. For eg, the Direct-to-consumer (D2C) sector generates a lower return than Software-as-a-service (SaaS) because of their different cost structures and will have a lower hurdle rate. A fund focused on seed-stage deals might have a higher hurdle rate than a Series B stage fund. -

Fund Life

Each fund has a life of 7-10 years, at the end of which the money has to be returned to LPs. Bala has to beat the hurdle rate within this time frame.-

The first 2-3 years, Bala's effort goes into identifying and investing in startups

-

The next 3-4 years go into building them

-

The last 2-3 years is when Bala tries to 'exit' the investments and make money

-

-

Deal Structure

While the LPs understand VC is risky, Bala has to show what steps he'll take to protect the downside of that risk. One way to do that is to invest in the startup in the form of preferred equity, not common equity. Preferred equity gives VCs the higher preference over common equity help by startup founders in case the startup shuts down and sells off its assets and technology (eww, that's a bit mean). Bala can also show that he'll include-

Clauses for voting rights on key decisions like selling the company or when to IPO

-

Anti-dilution clauses - if the startup raises the next round of funding at a lower valuation, the # of shares owned by the fund will be adjusted so that the fund continues to own the same % of the startup as before the round

-

-

Fees

For his effort and for expenses to run the fund, Bala will charge the LPs a 'management fee' which is around 2-3% of the fund value every year. From this amount, Bala will pay himself, the rent for the office and salaries to the analysts and admin staff he'll hire. -

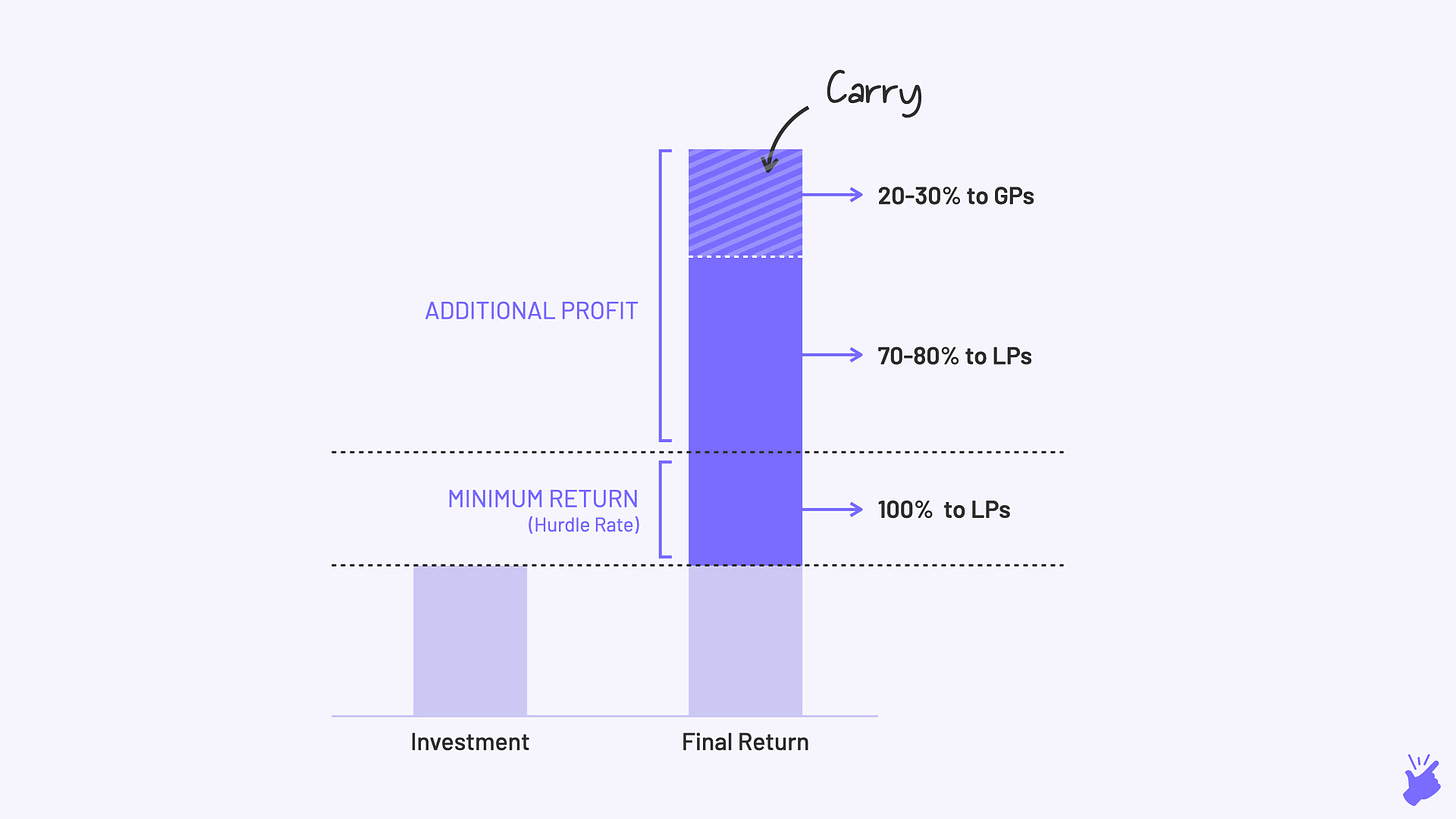

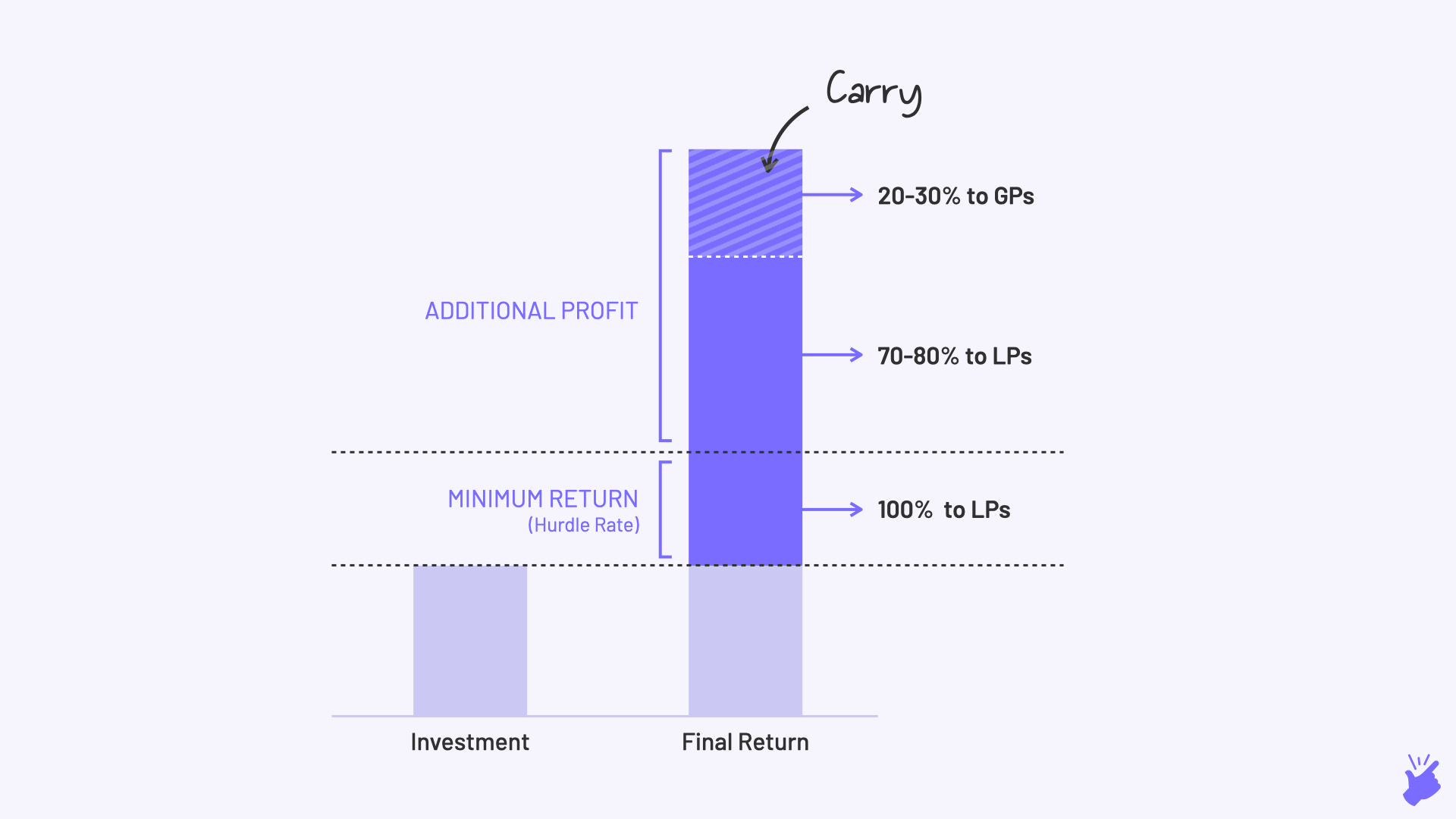

Carry

If Fee is the basic salary, Carry is the bonus that Bala will take home if the fund performs well. The profit generated by the fund over and above the minimum return promised is shared between the LPs (70-80%) and GPs (20-30% generally). This is to ensure Bala is incentivized to maximize the return of his fund. It is 'carry 'that will eventually form a large portion of Bala's earnings.

It's important to know that a typical VC firm has different funds within them. Each fund could have a different lifetime, different theme and different hurdle rate. And a different GP could be managing each fund. When you go through the list of portfolio companies on a VC's website, remember that they could be investments from different funds, each of which have different goals :)

VC is f**king tough

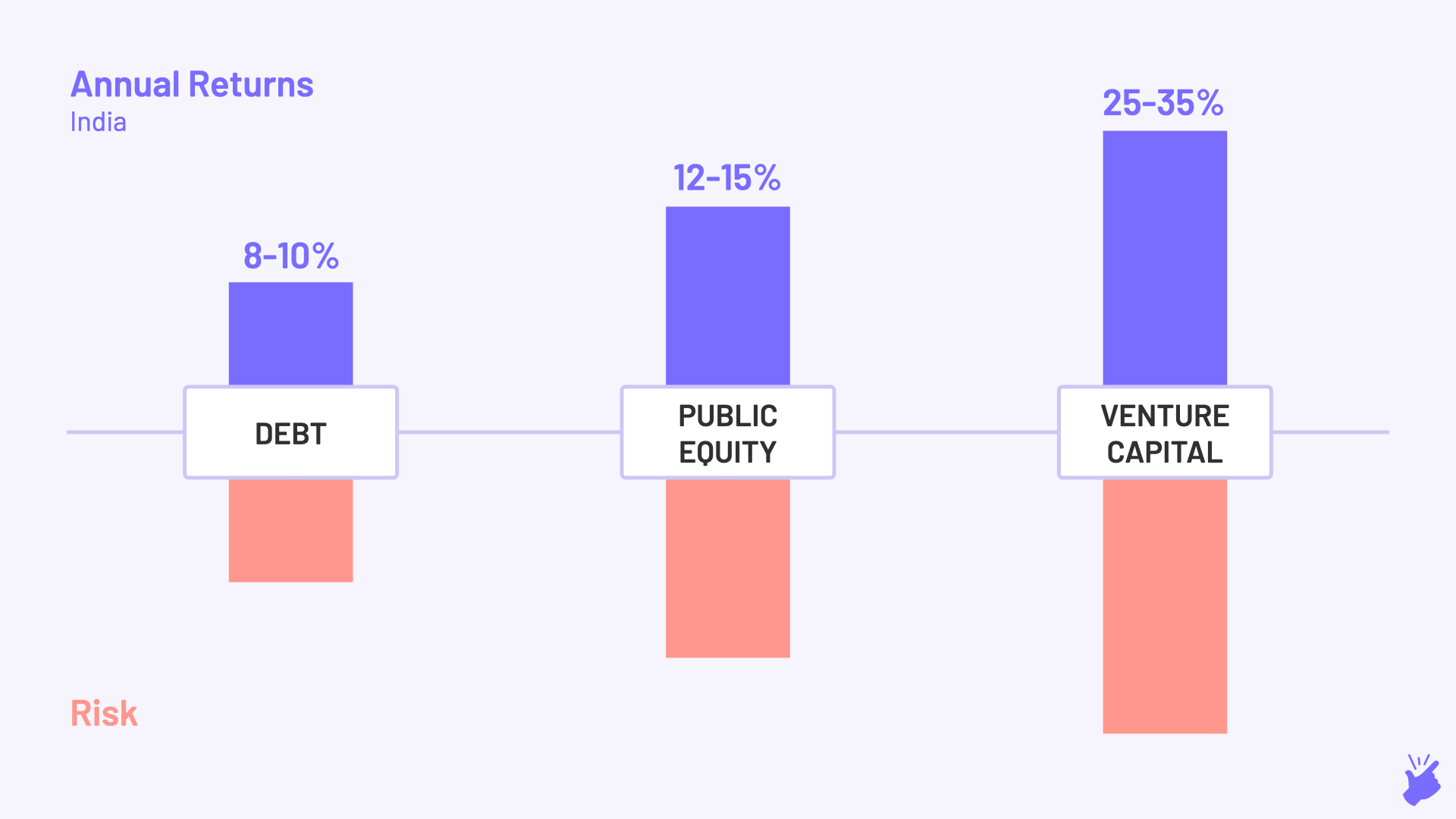

With high risk comes high returns. VCs are expected to generate a 25-35% annualized return compared to the 12-15% that public equity markets generate and much higher than the 8-10% return that debt markets give.

Continuing Bala's example...

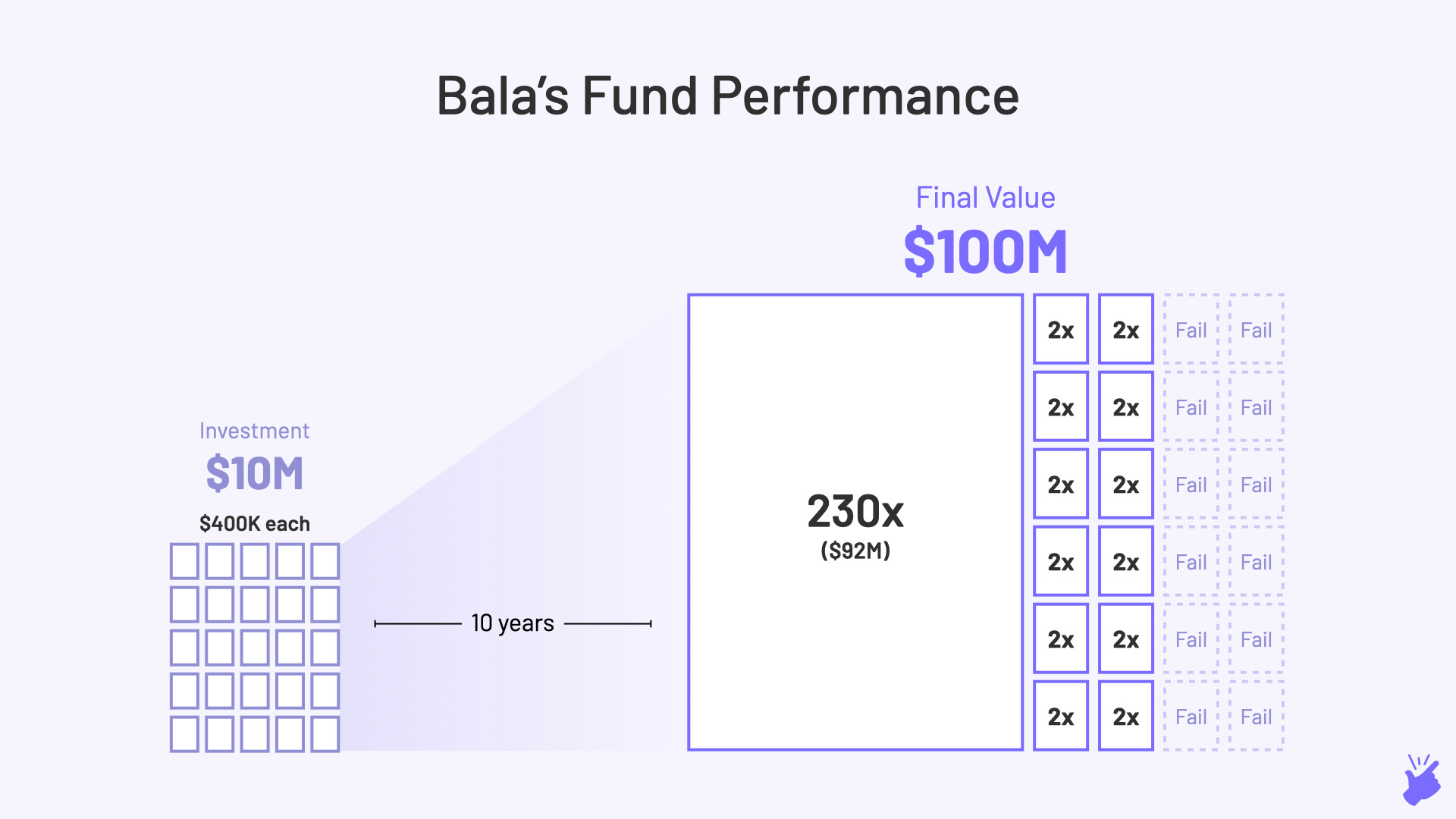

Bala ended up raising $10M and invested that money in 25 companies. To generate a 25% annualized return, Bala's fund has to at least 10x its original size, ie, the sum total of all the investments has to be at $100M (10x over 10 years = 25% year-on-year growth)

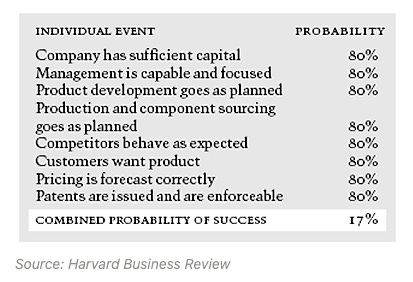

Now, this would have been simple if all the 25 startups grew 10x in those 4-5 years after Bala invested. But the problem is, that is rarely the case. In fact, 75% of venture-back startups fail. And it is not because VCs have bad decision-making skills. It is just really hard to build a successful company and even tougher to identify one very early in its lifecycle, however smart you are.

As you can see in the picture below, even if all the individual ingredients to building a successful company are at a high probability (80%), the overall chance of the company succeeding is only 17%. If even one ingredient is less like to happen (say 50% probability), the overall chance of the company succeeding drops to 10%.

So how do the VCs who make money actually make money?

VC returns work on something called the 'Power Law'. It basically means not all investments need to be a success. Just 1 or 2 successful investments can contribute to the return of the entire fund and make up for losses of all the others.

Out of the 25 investments by Bala, let's say 12 failed (zero value). And 12 grew only 2x (which is not enough). And 1 investment grew 230x. Then also, Bala's fund has managed to grow 10x and can be considered a success.

This is the kind of return that Oyo gave Lightspeed Ventures and Byju's is going to give Sequoia's India fund. Most VC funds don't generate that kind of return. In fact, they even end up losing money (less than 1x return).

What the power law implies…

Bala has to judge every company he's investing in from the lens of "Will this investment grow 200 times in the next 4-5 years?". It is this reason why VCs tend towards only companies that are going after large markets ($1B+) and have really high growth rates. Naturally, tech-centric companies fit the profile since they can grow very fast.

Ciao!

That's it for today. This turned out to be a marathon of an explainer. But I hope you got a fair understanding of how a VC fund works.

More reads on the topic...

-

The First Venture Capitalists: An interesting read on how the whaling industry of the 1800s was very similar to modern-day venture capital

-

Venture Capital and the Internet's Impact: A superb piece by Ben Thompson (a favourite of mine) on how VCs are getting squeezed. Traditionally, VCs invested in startups from idea to IPO. But due to the advent of the internet and few other new dynamics, angel investors are investing at the idea stage and public investors like Fidelity are investing at the just-before-IPO stage. This has left VCs with very little space in between.

from Hacker News https://ift.tt/3ejDfl6

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.